6 Corporate Transition to Net Zero

Saphira Rekker

Chapter Overview

At the end of this chapter you will be able to:

- Explain the concept of net zero and how it relates to the Paris Agreement

- Explain different global emissions reduction pathways, and their trade-offs, to meeting the goals of the Paris Agreement

- Discuss trends and challenges in relation to human development and climate change

- Explain how greenhouse gas emissions are measured on a corporate level.

You have probably heard the term “net zero”, perhaps from countries or companies aiming to achieve net-zero emissions by a certain date, commonly by 2050. In this chapter we will have a close look where the concept of “net zero” comes from, what it means, and how it relates to the goals of the Paris Agreement. We will dive deeper into carbon budgets, pathways to stay within those budgets, and how to assess the impact of businesses on climate. Hereby we continue our discussion in Chapter 4 including the concept of Climate Transition Risks faced by companies.

In this chapter we will encourage you to become familiar with important resources on climate change so you know where to find information in the future. In particular, we extensively draw upon the International Panel on Climate Change (IPCC), which collates the knowledge and science on climate change to date and consists of three working groups: Working Group I focuses on the physical science basis, Working Group II on climate impacts and adaptation, and Working Group III on climate change mitigation.

Net Zero and the Paris Agreement

As we covered in the prior chapter, the Paris Agreement is a globally significant agreement to limit global warming. It is important to go to the source itself to understand what the Paris Agreement states. Here is the link to the Paris Agreement (PDF, 4.33MB).

Here are some of the key elements of what the Paris Agreement states (2015, p. 2):

“Acknowledging that climate change is a common concern of humankind”.[1]

In other words, tackling climate change has nothing to do with the planet, the planet will still be here if humans are not! It is about maintaining life-supporting systems for humans, their activities and development – humans and other species are vulnerable and dependent on the functioning and state of our natural systems, specifically our climate.

“Article 2:

- This Agreement […] aims to strengthen the global response to the threat of climate change, in the context of sustainable development and efforts to eradicate poverty, including by:

- (a) Holding the increase in the global average temperature to well below 2°C above pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels, recognizing that this would significantly reduce the risks and impacts of climate change;

- (b) Increasing the ability to adapt to the adverse impacts of climate change and foster climate resilience and low greenhouse gas emissions development, in a manner that does not threaten food production; and

- (c) Making finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development.

- This Agreement will be implemented to reflect equity and the principle of common but differentiated responsibilities and respective capabilities, in the light of different national circumstances.”[2]

This is a key paragraph in the Paris Agreement. It highlights the temperature limit agreed upon, that development should integrate both adaptation and be low carbon, and that rich nations have a greater responsibility to address climate change. This last point reflects that rich countries have more capability to address climate change, but also recognises that these nations’ economic development resulted by them producing the majority of global emissions to date (we will discuss this further later in the chapter). This is what the climate negotiations at the Conference of Parties (COP) every year are about, nations coming together to discuss progress, commitments and responsibilities.

“Article 4: 1. In order to achieve the long-term temperature goal set out in Article 2, Parties aim to reach global peaking of greenhouse gas emissions as soon as possible, recognizing that peaking will take longer for developing country Parties, and to undertake rapid reductions thereafter in accordance with best available science, so as to achieve a balance between anthropogenic emissions by sources and removals by sinks of greenhouse gases in the second half of this century, on the basis of equity, and in the context of sustainable development and efforts to eradicate poverty.”[3]

This paragraph actually refers to net zero – the balancing of carbon sources with sinks. However, note that it is in the context of article 2, and needs to be paired with rapid reductions. It is not possible, at this point, to create enough carbon sinks to absorb our emissions. The pathways to net zero (how we will get to net zero) matters greatly, and is what we will discuss further in this chapter.

Carbon Budgets

Cumulative greenhouse gas emissions determine the concentration of carbon in the atmosphere, and in turn global temperatures. There are six main greenhouse gases emitted by human activities: carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs) and sulphur hexafluoride (SF6). These different greenhouse gases have different warming strengths, and different life spans. The most dominant and prevalent greenhouse gas emitted by human activities is carbon dioxide, which is also a very long-lived gas (there is no single estimate, but it is likely centuries, up to even 1000 years). Other gases, like methane, have a very high potency (up to 83 times stronger than CO2), but are relatively short lived (around 12 years). Greenhouse gases are often expressed as a carbon dioxide equivalent (CO2-e) to be able to understand their warming potentials.

Exercise

As part of its work on the physical science of climate change, Working Group I of the IPCC includes the latest estimates on the remaining carbon budget in its reports. The Remaining Carbon Budget is the amount of carbon that can be emitted, starting from a specified year, to remain within a certain temperature increase, from that year. This budget is an estimate and has a high uncertainty – it could be much higher or much lower. This is because of various factors; non-CO2 scenario variations; non-CO2 forcing and response uncertainty; historical temperature uncertainty and recent emissions uncertainty. For example, we don’t know at exactly what temperature the ice caps melt, and although we know there are large quantities of methane stored underneath that will be released, we only have an estimate. Given that some changes will be irreversible, it is important to take a precautionary approach and not take the risk that the budgets are larger than expected, but rather that they are smaller.

Here is your first practice to look up information in IPCC reports.

- Go to ipcc.ch. Click on Working Groups -> Working Group I -> AR6 Synthesis Report: Climate Change 2023

- If you can’t find it, go to AR6 Synthesis Report: Climate Change 2023 Technical Summary (PDF, 30.9MB) [4]

- Use Ctrl+F to search for “remaining carbon budget”.

Open Question: how many “hits” are there from searching for this term?

Answer:

29

- Find “Table TS.3 | Estimates of remaining carbon budgets and their uncertainties”.

- What is the estimated carbon budget from 2020 to have an at least 33%/50%/67% chance to keep global surface temperature change below 1.5°C/1.7°C/2.0°C since pre-industrial levels? And what are the variations based on non-CO2 and other uncertainties? Complete the table below:

| Global surface temperature change since 1850-1900 | Estimated RCB from 01/01/2020 (subject to variations) | Scenario variation | Geophysical uncertainties | |||||

|---|---|---|---|---|---|---|---|---|

| °C |

Percentile GtCO2 |

non-CO2 scenario variations | non-CO2 forcing and response uncertainty | Historical temperature uncertainty | Zero CO2 emissions commitment uncertainty | Recent emissions uncertainty | ||

| 33% | 50% | 67% | GtCO2 | GtCO2 | GtCO2 | GtCO2 | GtCO2 | |

| 1.5 | ||||||||

| 1.7 | ||||||||

| 2.0 | ||||||||

Answer:

| Global surface temperature change since 1850-1900 | Estimated RCB from 01/01/2020 (subject to variations) | Scenario variation | Geophysical uncertainties | |||||

|---|---|---|---|---|---|---|---|---|

| °C |

Percentile GtCO2 |

non-CO2 scenario variations | non-CO2 forcing and response uncertainty | Historical temperature uncertainty | Zero CO2 emissions commitment uncertainty | Recent emissions uncertainty | ||

| 33% | 50% | 67% | GtCO2 | GtCO2 | GtCO2 | GtCO2 | GtCO2 | |

| 1.5 | 650 | 500 | 400 | +- 220 | +- 220 | +-550 | +- 420 | +-20 |

| 1.7 | 1050 | 850 | 550 | |||||

| 2.0 | 1700 | 1350 | 1150 | |||||

- b. If we are looking to have a 67% chance to keep temperature limits to 1.5°C compared to pre-industrial levels, what is the remaining carbon budget from 01/01/2020?

Answer:

400 GtCO2

- Now we are going to retrieve information from another IPCC report. Go to ipcc.ch. Click on Working Groups -> Working Group III -> Reports -> Summary for Policymakers

- If you can’t locate it, go to IPCC Climate Change 2022 – Mitigation of Climate Change – Summary for Policymakers (PDF, 1.11MB)[5]

- a. What were the global net GHG emissions in 2019? (Hint: see item B.1.1)

Answer:

59+- 6.6 GtCO2-e

- b. What were the net CO2 emissions from fossil fuel combustion and industrial processes (CO2 FFI) in 2019? (Hint: see figure SPM.1)

Answer:

38+- 3 GtCO2

- c. What were the net CO2 emissions from land use, land-use change and forestry (CO2 LULUCF) in 2019? (Hint: see figure SPM.1)

Answer:

6.6 +-4.6 GtCO2

- d. If you compare the sum of net CO2 (not CO2-e, so the sum of CO2 FFI and CO2 LULUCF) against the carbon budget we calculated previously (400 GtCO2 to have a 67% chance to remain within 1.5°C)[6], and if emissions were not reduced, in what year would we would reach 1.5°C?

Answer:

2029 (remember the carbon budget is from 2020). The answer is calculated by 400/(38+6.6) =8.97 + 2020, so in the 9th year after 2020.

Hopefully the prior exercise has given you a good overview of carbon budgets and the challenge ahead.

Carbon Dioxide Emissions Pathways

As we saw before, to have a more than 50% chance of staying below 1.5°C, cumulative emissions need to be kept within 500 GtCO2 from 2020, which is also referred to as the “remaining carbon budget”. Currently, we emit around 40-45 GtCO2 globally every year. As you calculated in the exercise above, this means that if we do not reduce emissions, we could exceed the budget before 2030. The IPCC outlines different pathways to reduce emissions society can follow, all resulting in net zero CO2 emissions around 2050.

Exercise

We are going to open some IPCC reports again. First, we are going to have a look at the special 1.5°C report that was published in 2018, specifically the Summary for Policymakers. Try finding it yourself on ippc.ch, If you can’t find it, go to IPCC Summary for Policymakers (PDF, 799KB).[7]

On page 14 you can find four illustrative pathways to limit global warming to 1.5°C. Have a look at the indicators that are paired with each pathway.

All scenarios require a fundamental shift in the energy sector away from fossil fuels, requiring large investments in renewable energy and storage solutions and a loss of value of existing fossil fuel assets. The scenarios also all rely on AFOLU (Agriculture, Forestry and Other Land Use) emissions, such as afforestation (e.g. planting trees), to go to zero and turning negative using Carbon Dioxide Removal technologies, that remove carbon from the atmosphere. Three of the four scenarios also include removal of carbon through Bioenergy with Carbon Capture and Storage (BECCS). These technologies however have many limitations, one of which is a high cost.

The first scenario (P1), assumes low population growth, with reduced energy demand and rapid decarbonisation, which is depicted by the rapid decrease of fossil fuels. In contrast, the last scenario (P4) depicts high population growth and high consumption patterns, where population remains reliant on fossil fuels. Although there is a reduction in the amount of fossil fuels (grey area), it still remains largely present for the next few decades. This scenario will need to rely heavily on technologies such as carbon capture and storage (CCS).

In the most recent report in 2023, more Illustrative Mitigation Pathways (IMP) were added in addition to the Shared Socio-economic Pathways in the 2018 report. You can view these IMPs in Figure SPM.5 on page 26-27 of the report – IPCC Climate Change 2022 – Mitigation of Climate Change – Summary for Policymakers (PDF, 1.11MB).

Panel E shows the different carbon sources and sinks associated with each pathway at the time of net zero.

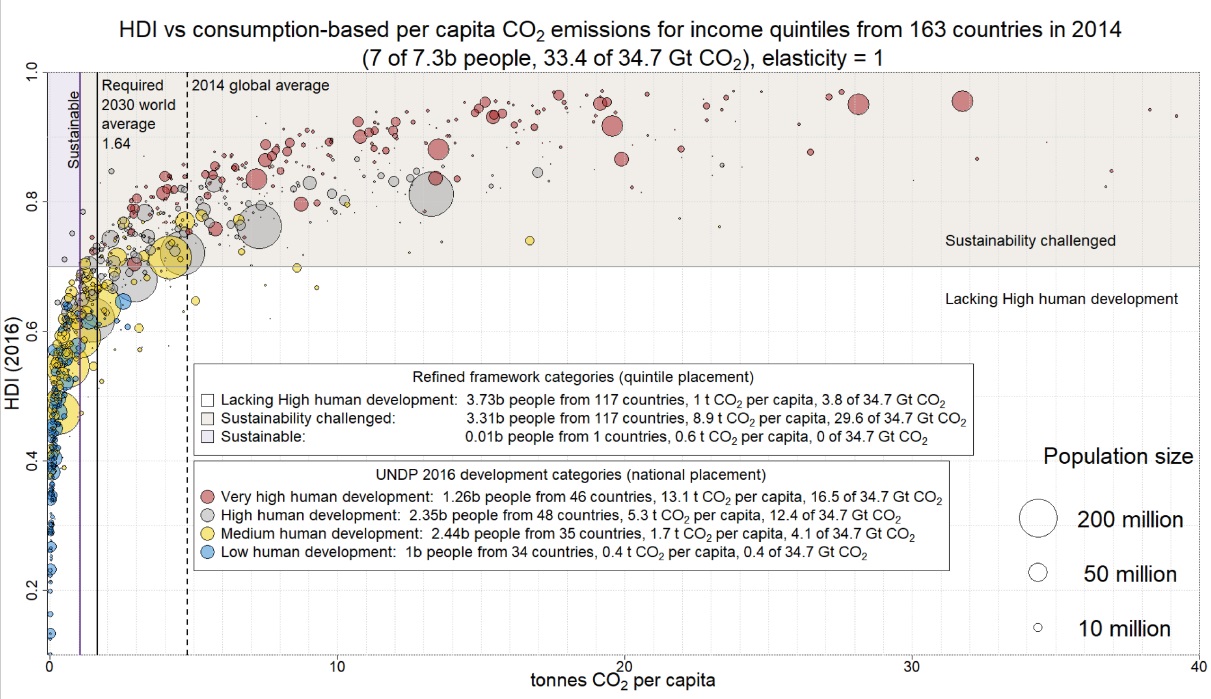

Human Development Index

The climate challenge can also be seen as a “dual-challenge”. The figure below looks at the correlation between HDI (Human Development Index) and consumption-based per capita CO2 emissions, considering different income quintiles.

From the graph you can see a clear trend: the higher the development, the higher the carbon emissions per capita. For example, if you live in Australia on an (relatively low) income of around A$25,000 per year, then your carbon footprint is estimated to be around 13 tonnes of CO2. This amount can vary depending on a couple of factors, including one’s travelling habits (e.g. international flights), as well as diet (e.g. vegetarian or meat-based diet).

If everyone in the world was given an “equal” carbon budget, how much would this be? In order to stay within a 2°C consistent carbon budget, everyone in the world would have 1.64 tonnes of CO2 allocated per person to emit in 2030. Compare this to the 13 tonnes of CO2 emitted by someone in Australia earning A$25,000 per year. The challenge for developed countries is therefore to maintain a high HDI, but decrease the emissions per capita. For developing or underdeveloped countries the challenge is quite different, as they currently have very low CO2 levels per capita. Their challenge is to increase their HDI without increasing their emissions. As we saw at the beginning of the chapter, an important element of the Paris Agreement is that there are “common but differentiated responsibilities”. This means that because developed countries have emitted by far the largest portion of emissions, and have benefited from this greatly, they have a greater responsibility in mitigating climate change, which also included providing Climate Finance to poorer countries.

Carbon Intensity Pathways of Sectors: How Can We Decarbonise Different Sectors?

In order to contribute to the CO2 reduction process, industries have to adopt significant transformations. Have a look at Table 2 of this Nature Climate Change article[8], which provides a summary of the unit reduction certain industries have to achieve in order to achieve the sustainability targets.

For example, in the case of power generation, the global average was 591 g CO2 per kWh 2011 and to stay within a global carbon budget consistent with staying below 2°C, this amount should be reduced to 28.7 by 2050. Power generation currently predominantly relies on the use of fossil fuels. Ways to decarbonise power generation can be achieved with renewable energy or nuclear power. However, both options carry certain risks or drawbacks. An increase in renewables has to be paired with investment in energy storage and smart systems. There is some exciting research ongoing by UQ researcher Dr Jake Whitehead on using electric vehicles as portable energy storage systems, i.e. “battery-on-wheels”.

Climate Change as a Tragedy of the Commons

Climate change can be seen as a classic example of a “tragedy of the commons”. This occurs where a common pool of resources is overexploited. Globally, individual entities (each country, each company, and each individual) have a self-interest to consume or produce more than their “fair share” of greenhouse gas emissions, which has led to a suboptimal state of our common climate. Think “why should I fly less when all my colleagues or friends don’t? Why should I consume less energy when everyone else doesn’t?” (for more information on the tragedy of the commons, please have a look at The Tragedy of the Commons published in Science).

Solving this issue requires collective action, and it is essential to recognise the importance of governance, ethical dimensions, equity, value judgments, economic assessments and diverse perceptions and responses to risk and uncertainty. Hardin (1968)[9] argues that there is no technical solution to the tragedy of the commons. It requires education , recognising the necessity to give up a little bit of freedom by regulating the commons and reducing the production of greenhouse gases, because only then can people be “free”; “But what does “freedom” mean? When men mutually agreed to pass laws against robbing, mankind became more free, not less so. Individuals locked into the logic of the commons are free only to bring on universal ruin; once they see the necessity of mutual coercion, they become free to pursue other goals.”[10]

Nobel Prize winner in economics, Elinor Ostrom[11], however, argued that Hardin’s (somewhat depressing) view did not line up with how we observe humans behave. Her work argues that in reality, the tragedy of the commons can be overcome by cooperation and self-regulation i.e. by groups coming up with agreed ways to divide up a resource. You can see a direct link between her ideas and some of the collaborative initiatives we discussed in Chapter 3 as well as the Paris Agreement. You can read more about Elinor Ostrom in the article published in Nature.

Climate change was first addressed internationally as a major issue in the 1970s, in an IPCC report. Since then, there have been numerous international negotiations on how to solve it, mainly evolving around which country has to do what, which highlights this case as a collective action problem.

Did You Know?

There is an increasing area of the law that deals with the rights of people in regards to climate change.

For example, in the Netherlands, there was a lawsuit brought by citizens who sued their government for not taking enough action against climate change. They won the first case, which was appealed, and then they won again. This initiated an international breakthrough in terms of law, encouraging courts to mandate that governments take the required actions.

What do you think about the role of educators, and universities? Do you believe they have a big influence in this case?

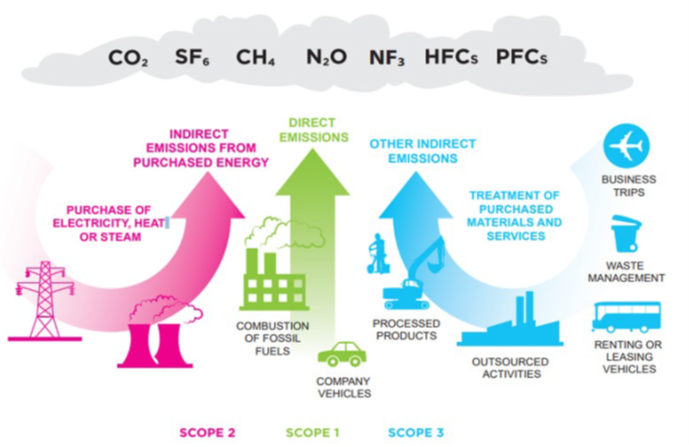

Corporate Carbon Accounting – GHG Protocol

We have covered different emission sources and global emissions accounts, but accounting for a company’s emission requires a specific approach. The international guidelines on how to account for a company’s emissions can be found by the Greenhouse Gas Protocol. The GHG Protocol classifies companies’ greenhouse gas emissions into three types as follows:

- Scope 1 emissions: direct emissions from owned or controlled sources. Examples are fugitive emissions (e.g. gases escaping from a mine) and livestock emissions (e.g. anaerobic digestion from livestock)

- Scope 2 emissions: indirect emissions from the generation of purchased energy

- Scope 3 emissions: all indirect emissions (not included in scope 2) that occur in the value chain of the reporting company, including both upstream and downstream emissions.[12] Scope 3 covers a wide range of emissions and are divided into 15 categories:

- Downstream:

- purchased goods and services

- capital goods

- fuel- and energy-related activities

- upstream transportation and distribution

- waste generated in operations

- business travel

- employee commuting

- Upstream:

- upstream leased assets

- processing of sold products

- use of sold products

- end-of-life treatment of sold products

- downstream leased assets

- franchises

- investments

- Downstream:

Concept Check

Let’s look at a few examples to illustrate how it works.

Exercises

Question: The company Energise owns a facility that uses 10,000 tonnes of coal for the generation of electricity. How should the emissions from the coal combustion be recorded (Scope 1, 2 or 3)?

Answer:

Scope 1. The facility is owned by the company and is generating direct emissions.

Question: The University of Oceanic Views (UOV) owns a facility that produces 200 tonnes of solid waste, which was collected by the local council to go to landfill. How should UOV record the emissions associated with its landfill?

Answer:

Scope 3: Waste generated in operations. These are indirect emissions for UOV. The organisation that owns the landfill facility will have to record it as direct emissions. Note that this means there is double counting in the economy (one organisation’s Scope 1 emissions become another organisation’s Scope 3 emissions); however, it allows for shared responsibilities and the accounting of risks for both parties.

Question: The freight company NotElectricYet uses 25,000 kL of diesel to operate its fleet. How should the company record the fuels purchased?

Answer:

Scope 1. The company owns the vehicles it operates, and they directly emit CO2 through the combustion of the fuels.

Question: The company BnB consumes 100,000 kWh of purchased electricity from the grid. How should this electricity be recorded?

Answer:

Scope 2. Purchased electricity falls under Scope 2.

Measuring and recording a company’s emissions is only the very first step in managing a company’s GHG emission and climate risk. To effectively manage a company’s transition risk, increasingly companies are being asked to align with the goals of the Paris Agreement. Under its core component of transition risk, “metrics and targets”, the TCFD[13] recommends companies to disclose the following:

- whether the target is absolute or intensity based

- time frames over which the target applies

- base year from which progress is measured, and why

- key performance indicators used to assess progress against targets.

Further, in 2021 Larry Fink, the CEO of Blackrock, asked in his annual letter to CEOs to “disclose a business plan aligned with the goal of limiting global warming to well below 2°C, consistent with achieving net-zero global greenhouse gas emissions by 2050”.[14] Regulators across the world are increasingly requiring companies to disclose their targets, the progress against them and even to meet certain emission reduction levels.

Science Based Targets

Following the Paris Agreement, several organisations came together to develop the Science Based Targets initiative (SBTi). This initiative was to set global guidelines on aligning corporate emission reduction targets with the Paris Agreement. It was founded by the Carbon Disclosure Project, UN Global Compact, World Resources Institute and World Wide Fund for Nature.

Fast forward, in January 2024 over 7000 companies are “taking action” through the initiative. The SBTi provides several guidelines, including sector-specific methods. It requires companies to set near-term targets (between 5-10 years), and optional long-term targets. These targets are then also listed on the SBTi’s website.

In simple terms, there are two different methods:

- Absolute Contraction Approach (ACA). This approach requires every company to reduce their emissions by the same % every year, year on year.

- Sectoral Decarbonisation Approach (SDA). This method takes a sectoral approach to allocating the carbon budget. It takes global sectoral reduction pathways, which outline sectoral emissions as well as demand/production, and then determines a companies’ required emission reductions based on its initial carbon intensity and its market share over time.

The SBTi provides tools on their website to help companies to develop targets.

Review Questions

Complete the chapter review questions below to test your knowledge.

- United Nations. (2015). Paris Agreement. https://unfccc.int/sites/default/files/english_paris_agreement.pdf ↵

- Ibid, p.3 ↵

- Ibid, p.4 ↵

- Intergovernmental Panel on Climate Change. (2023). AR6 synthesis report: Climate change 2023: Technical summary. https://www.ipcc.ch/report/ar6/wg1/downloads/report/IPCC_AR6_WGI_TS.pdf ↵

- Intergovernmental Panel on Climate Change. (2022). Climate Change 2022: Mitigation of climate change: Summary for policymakers. https://www.ipcc.ch/report/ar6/wg3/downloads/report/IPCC_AR6_WGIII_SummaryForPolicymakers.pdf ↵

- The reason we use CO2 only is because the other gases have shorter life spans and therefore also other mitigation pathways, so these non CO2 gases were included in the uncertainty estimates you completed in the prior exercise. ↵

- Intergovernmental Panel on Climate Change. (2018). Summary for policymakers. https://www.ipcc.ch/report/ar6/wg3/downloads/report/IPCC_AR6_WGIII_SummaryForPolicymakers.pdf ↵

- Krabbe, O., Linthorst, G., Blok, K., Crijns-Graus, W., van Vuuren, Detlef P., Höhne, N., Faria, P., Aden, N., & Pineda, Alberto C. (2015). Aligning corporate greenhouse-gas emissions targets with climate goals. Nature Climate Change, 5(12), 1057-1060. https://doi.org/10.1038/nclimate2770 ↵

- Hardin, G. (1968). The tragedy of the commons. Science, 162(3859), 1243-1248. http://www.jstor.org/stable/1724745 ↵

- Ibid. ↵

- Janssen, M. A. (2012). Elinor Ostrom (1933–2012). Nature, 487(7406), 172-172. https://doi.org/10.1038/487172a ↵

- Greenhouse Gas Protocol. (n.d.). FAQ. https://ghgprotocol.org/sites/default/files/standards_supporting/FAQ.pdf ↵

- Task Force on Climate-Related Financial Disclosures. (2017). Metrics and targets. https://www.tcfdhub.org/metrics-and-targets/ ↵

- Fink, L. (2021). Larry Fink's 2021 letter to CEOs. BlackRock. https://www.blackrock.com/us/individual/2021-larry-fink-ceo-letter ↵