Chapter 7: Cost Planning Stages

7.0 Introduction

This chapter explains the cost planning stages as per the Australian Cost Management Manual Volume 1 (AIQS, 2022) and the Elemental Analysis of Costs of Building Projects (NZIQS, 2017). Cost planning is given much emphasis in the cost management process in Australia and New Zealand and knowing the standard process and industry insights is very important for construction professionals. Chapter 6 introduced the major items to be considered in a cost plan, and this chapter presents their applications in each cost planning stage with real-life examples and lessons learned.

7.1 Cost planning process in the Australian context

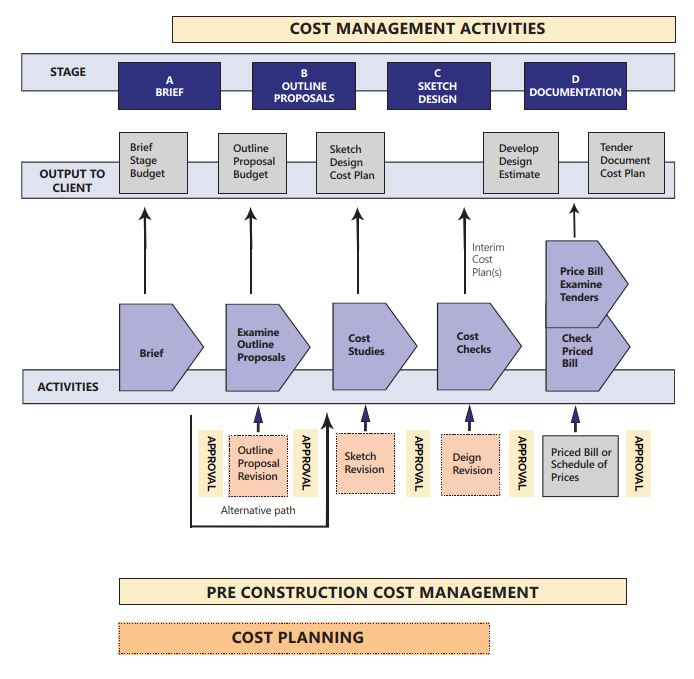

ACMM presents a construction project's cost management activities under 6 stages (Stage A to Stage F) and demonstrates them in a line diagram. Figure 7.1 is an extract from this line diagram showing the pre-construction cost management and cost planning activities (the complete line diagram is available in Appendix A). As provided in Section 2.3.2, ACMM explains cost planning as the application of cost management to the design process from the Brief Stage (Stage A) until the Tender Documentation Stage (Stage D). After Stage D, tendering will take place and construction will begin. The focus of this textbook is on cost planning, and therefore, Stage A to Stage D will be explained hereinafter referring to this line diagram.

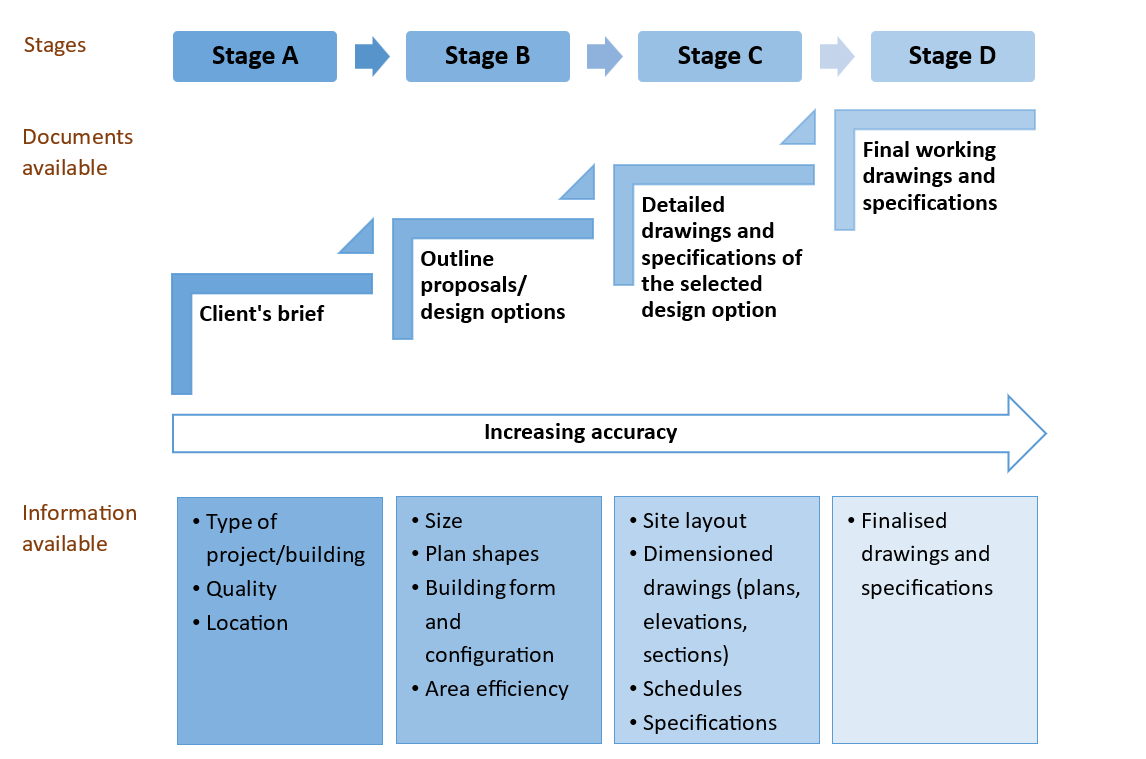

The accuracy of a cost estimate will usually increase with the level of information available. A construction project involves a range of documents, including drawings, specifications, schedules and other reports (e.g. soil investigation report). More detailed documents will be available in each progressive project stage. As the cost planning process evolves with the design development, the accuracy and certainty of estimates will be increased with the availability of information (see Chapter 6). Based on the information available, suitable cost planning techniques (see Chapter 3) can be applied. Before discussing each stage, Figure 7.2 presents an overview of the documents generally available, information used, and suitable cost planning techniques in each cost planning stage of ACMM.

In the industry practice, these stages are also specified as concept design, schematic design, tender design and detailed design.

Best practices for cost planning

During the cost planning process, reconciliation in the form of comparison of cost items between 2 stages (See Section 7.2) helps identify the impacts of design development on project costs. It is a part of Tender Document Cost Plan (Stage D) as per ACMM. This can also be done simply in other stages to see the impact of design/scope changes to the cost.

Value management studies are also carried out to give the best value for client's money and to maintain the end project cost within the budget, by comparing alternative designs, materials, methods and so on.

Cost planning activities in each stage are detailed hereinafter.

7.1.1 Brief (Stage A)

AIQS (2022, p. 2) defines the Brief Stage Cost as 'a first cost indication to the client based on an outline statement of the client’s needs. The indicative cost is intended only as a guide for feasibility’ and planning purposes; it is not an estimate and should not be quoted as such'.

The major purposes of this stage can be establishing the initial budget or to confirm that the Client’s budget is feasible. It indicates the Client's financial commitment and affordability. Therefore, it determines the continuation of the project and subsequent cost planning (whether to continue or not with the project).

In actual projects, Stage A can involve further developed design information cost plans.

Documents available

- In this initial stage, the Client's brief is used as the basis to produce an indicative cost.

- The Client's brief can be an outline statement of the Client's needs.

- Drawings are usually not available in this stage.

- Any available sketches and information will be used.

Information used

- Type of building/project: The type of building is always related to its purpose and function. This help identify the specific requirements of a project.

- Types can be residential, commercial, office building, hospitals, schools, stadiums and so on.

- Quality: Some building types can be categorised based on their quality. This is usually done based on the level of services provided in relation to its primary function during the operational stage of the building. The building should be completed in a way to facilitate that level of service.

- Hotels can be categorised with star grades (5-star, 4-star).

- Offices can be categorised as Premium, A-grade or B-grade.

- Location: Even with the same building design and materials, the cost of 2 projects can differ due to their location.

- Project areas such as in a central business district (CBD), city fringe, suburban areas.

- Space requirements: Although the design and building layout is not decided, the client will probably have an idea of the size of the project to be.

- This can be indicated in the number of functional units, and/or floor areas (lettable office area/useable floor area).

- Any available project specific information will be used in this stage.

The common industry practice in Australia is to provide the functional area schedule in the Stage A cost plan. It is generally used at the Master Planning Stage of the project.

Master plan documents are prepared by main consultants and sub-consultants. They define the scope of work.

7.1.2 Outline proposals (Stage B)

The purpose of this stage is to identify the best means of satisfying the client’s requirements by comparing alternative proposals. The selected proposal will be the basis for cost planning in the next stage.

Documents available

- Outline proposals and/or design options prepared by the architect or design team (several outline proposals might exist).

Information use

- Project description (in this stage, more information will be available compared to the Client's brief in Stage A) (see Figure 7.2).

- Scope of the works related to the size, plan shape of the building, etc.

- Alternative designs can be available for building configuration, form and area efficiency.

- More information on functional areas.

- Building services plan drawings.

7.1.3 Sketch design (Stage C)

The purpose of this stage is to confirm and set the final budget. Therefore, it is prepared based on the approved design produced by the project design team based on the selected outline proposal in Stage B. This cost plan provides the client with an estimate of the total end cost of the project, identifies any risks to achieving completion of the project within the overall project budget and identifies any opportunities for further development of the cost plan at the completion of the design development phase of the project.

Documents available

- Site layout, including contours and external works information (extent of roads, paths, landscaping, service mains, covered ways, fencing, etc.).

- Dimensioned sketch plans, elevations, sections.

- Structural sketches with dimensions of members and details.

- Schedule of finishes.

- Specification notes.

- Building services design and specifications.

Information used

Alternative construction methods, materials and systems will be considered to ensure that the overall design is the most effective. This can be done by establishing elemental cost benchmarks (see Section 4.3). Cost planning can be performed using elemental breakdowns with specific construction methods and materials.

Although the overall design in terms of building shape, plan size and building configuration is finalised when moving from Stage B to Stage C, the design in terms of methods and materials such as specific finishes and services can be further analysed and refined to meet the budget. Elemental breakdown with specific methods and materials will be important in this task.

Interim cost plans may be prepared in this stage before finalising the design and to maintain the costs within the budget. Thereafter, the final tender document cost plan can be prepared in Stage D.

Remember the difference between cost and the budget? (See Section 2.2)

7.1.4 Tender document cost plan (Stage D)

Tender Document Cost Plan (Stage D) is used at the documentation stage of the project getting ready for tendering. This stage will provide a detailed cost plan with finalised construction drawings and specifications. This cost plan is also based on accurate assessments of marketplace cost conditions and escalation.

There may be several other important activities in this stage to ensure that the overall design is contained within the budget:

- Comparison with cost plans in previous stages will be carried out to report on the variances in the form of Reconciliation Statements (see Section 7.3). This enables the design team to be aware of the cost implications of the design to ensure the completed design is contained within the agreed cost limit/budget. It also facilitates comparisons in elemental basis to meet elemental cost limits. This is a common practice in government projects.

- Cost checks on major elemental or area measurements and elemental costs is another important activity in this stage. Some rules of thumb can be used for this based on the experience of cost planners. Examples are presented later in this chapter.

Example: Cost checks

Cost checks can be carried out by comparing major elemental quantities for accuracy. Any differences have to be identified with reasons. Such comparisons can include the following:

- Substructure (SB) + Upper Floors (UF) and Fully Enclosed Covered Area (FECA)

- Ceiling Finishes (CF) and FECA

- Floor Finishes (FF) and FECA

- External Walls (EW) + Internal Walls (NW) × 2 and Wall Finishes (WF) (this element refers to internal finishes)

Note: These elements, elemental codes and area measurements are as per ACMM. Measured examples are available in Chapter 8.

The following ratios can also be checked:

- [External Walls (EW) + Windows (WW)] / FECA

- WW / (EW + WW)

Documents available

- Final working drawings and specifications.

- Engineering services cost plans.

Information used

- All the details of the project necessary for cost planning will be available at this stage with more accuracy.

7.2 Cost plans with a sample project

This section presents an example hospital project in Australia to demonstrate cost planning in each stage. The project is now completed, but this explains the steps carried out during design development and cost planning process.

Example: Hospital project

Project information

Project title: ABCD Hospital Redevelopment in Melbourne

Client: The Department of Health, Victoria, and a Health Services facility

Scope of the project: The project consists of the new build construction of a hospital building, together with significant earthworks to raise site levels and the construction of a separate ambulance station.

Budget: The approved funding and budget for the project was $22.7 million. There is no surplus or deficit in the current approved budget.

Project milestones

- Out to tender: mid-January 2013

- Construction start date: 15 April 2013

- Construction completion: 15 August 2014

Reference documents

- Department of Health Project Brief

- Australian Cost Management Manual

- Department of Health, Capital Works Guidelines

Assumptions

The term cost estimate is used in this section, but it should not be confused with Builder's estimates (see Section 6.1).

- Cost estimates assume that a traditional procurement route will be adopted for the project and which will be competitively tendered to achieve a fixed price lump-sum for each element of the works.

- Cost estimate also assumes that the project will be constructed as a single stage construction.

- No allowance is included for any additional costs associated with adopting non-traditional forms of building procurement.

- If a ‘cost-plus’ or similar route is adopted, or if a sufficient quantity of suitable tenderers cannot be achieved within the marketplace, then it is likely that a cost premium will be realised and must be added to the budget.

Cost plan A

In this example, cost planners prepared this in the Brief Stage (Stage A) based on functional/departmental areas of the hospital. Chapter 3 also provides a simple example of a cost plan based on the functional areas for a boarding house project.

Documents used as the basis of the Cost plan A

Sketch drawings and documents, which were available on May 2012, were used for this cost plan, including:

- master plan sketch drawings (There were several options of master plan sketches available to consider at this initial stage.)

- proposed schedule of accommodation (functional areas)

- the master plan estimate for services provided by the services consultant

- no separate structural or civil drawings were available.

Basis for measurement and pricing

- Cost estimates were based on area measurements taken from architectural drawings adopting historical costs of similar projects from the project's cost consulting company's database of health project costs.

- Functional area method is the cost planning technique used here. These are also known as 'departmental areas'.

- Building Services costs have been incorporated with departmental area rates while External Services are shown separately as project specifics. Both costs are from engineering cost estimates based on the advice from the services consultant.

- Costs of Central Energy Systems, Infrastructure Services and External Services are project-specific estimates based on the advice from the services consultant. This cost also includes any infrastructure upgrades required for the continuation of the project (i.e. ACMM element of Work to utilities off-site (see Section 6.4.2).

- Cost estimates were based on the current rates at the time, including site and locality allowances (see Chapter 4) as at May 2012 (BPI 190).

Preliminaries

- Preliminaries related to building works are captured within the departmental area rates.

- Preliminaries related to site works are calculated at a percentage.

Project specifics

- In addition to the common items such as site works, landscaping and services, this project needs to consider environmentally sustainable (ESD) initiatives.

- ESD allowance is calculated as 2.5% of building costs.

- Also, there is a specific requirement to fill the site area with suitable materials above the flood level.

Special provisions

Based on Department of Health Guidelines, allowances have been included for:

- Design Contingency at 5.0%

- Construction Contingency at 5.0%

- Escalation to tender issue (evaluated separately)

- Escalation to completion (evaluated separately)

- Locality allowance for building works has been included in the benchmark rates

- Locality allowance for site works has been calculated at a percentage.

Other project costs

- Other project cost items are calculated using appropriate percentages.

- Consultant fees are calculated using an appropriate amount.

Exclusions

- Land acquisition cost is not included in this cost plan at this stage.

- Demolition of old hospital is funded separately and is not included in this cost plan at this stage.

- Project Prolongation Contingency.

- Allowance Temporary Accommodation for the Hospital,

- Hospital Operations Costs.

- Impact of Carbon Tax.

- GST.

Cost plan A summary

Date of Cost plan A: 20 May 2012

| Project Component | Area (m2) | Rate ($/m2) | *Total 1 |

| Administration | 163 | 3,345 | 546,000 |

| Bed-Based Services | 858 | 3,894 | 3,342,000 |

| Emergency Department | 76 | 3,956 | 301,000 |

| Support Services | 462 | 3,638 | 1,681,000 |

| Primary Health | 658 | 3,337 | 2,196,000 |

| Medical Clinic | 278 | 3,683 | 1,024,000 |

| Ambulance Station | 217 | 3,280 | 712,000 |

| Subtotal - Gross Departmental Area | 2,712 | 3,615 | 9,802,000 |

| **Interdepartmental Travel (10%) | 272 | 2,434 | 662,000 |

| Subtotal - Gross Building Area | 2,984 | 3,507 | 10,464,000 |

| Project Specifics | |||

| Central Energy & Infrastructure Services | 2,990,000 | ||

| ***Site Works including Landscaping | 2,066,000 | ||

| External Services | 387,000 | ||

| ESD Initiatives | 2.5% | 262,000 | |

| Allowance for flood Resilience Works | 351,000 | ||

| Net Construction Cost | 5,537 | 16,520,000 | |

| Special Provisions | |||

| Design Contingency | 5.0% | 826,000 | |

| Construction Contingency | 5.0% | 826,000 | |

| Project Prolongation Contingency | Excluded | ||

| Total Construction Cost | 6,090 | 18,172,000 | |

| Other Project Costs | |||

| Fittings, Furniture & Equipment (FF&E) | 8.0% | 1,454,000 | |

| IT & Communications & Audio-visual Equipment | 5.0% | 909,000 | |

| Consultant Fees | 1,483,000 | ||

| Authority Charges, Headwork Fees, etc. | 0.6% | 110,000 | |

| Agency Management Support/Administration | 0.8% | 137,000 | |

| Department of Health (DH) Management Support/Administration | 0.8% | 137,000 | |

| Total Project Cost (@ May 2012) | 7,508 | 22,402,000 | |

| Escalation To Tender (evaluated separately) | 109,500 | ||

| Escalation To Completion (evaluated separately) | 188,500 | ||

| Land Acquisition | Excluded | ||

| Total Project End Cost (Excluding GST) | 7,608 | 22,700,000 | |

| Allowance for Demolition of Old Hospital | 400,000 |

1 Totals are rounded up to the nearest 1,000 multiples.

Details of site works

Site Specific Allowances have been included.

| Site Preparation & clearance | 77,000.00 |

| Building Demolition | 30,000.00 |

| Rock Removal | 20,000.00 |

| Removal of Contamination material | 20,000.00 |

| Roads and Paths | 350,000.00 |

| Carparking (50 cars) | 400,000.00 |

| Ambulance turning bays/Carpark | 120,000.00 |

| Road sealing work | 50,000.00 |

| Walls & Fences | 60,000.00 |

| External pedestrian steps/ramp footpath (Extraover Allowance) | 60,000.00 |

| Entry Canopy | 96,000.00 |

| Fire Water Storage | 140,000.00 |

| Garden Sheds | 22,000.00 |

| Service Vehicle Shed | 210,000.00 |

| Landscaping | 206,000.00 |

| Subtotal | 1,861,000.00 |

| ****Preliminaries & Locality Allowance on Site Works (11%) | 205,000.00 |

| Total Site Work | 2,066,000.00 |

Learnings from sample Cost plan A

Functional/Departmental areas

As the detailed drawings are not available at this stage, cost planners use sketches or approximation of functional areas. These are also known as 'departmental/accommodation areas'.

*Rounded figures

The amounts are rounded up to the nearest 1,000 multiples. This is a general practice of using approximate figures in early stage cost plans. This will indirectly increase the figures to cover any risks. However, more accurate figures will be used in later stages with the availability of more accurate project information.

**Interdepartmental travel

As the layout of functional areas are not finalised at this stage, a percentage allowance (10% in this example) is made for the circulation areas between the functional areas to obtain the total building area. In this cost plan, it is called 'interdepartmental travel areas'. As per ACMM, Interdepartmental travel includes links, wall thickness, lifts and plant areas are included in the project.

Rates of various functional areas

Rates per m2 of various functional areas have been applied. As mentioned in Chapter 4 and Chapter 5, benchmark rates can be derived by cost analysing similar previous projects .

Per gross area rates

Per gross building area rates are calculated for each subtotal. This provides a benchmark rate to have a better idea of the cost of the overall project in comparison to previously completed projects.

****Preliminaries & locality allowance on site works

A single figure has been used to capture preliminaries and locality allowance for site works. Such practices are common in early stage cost plans, where the purpose is to capture all cost items for budgeting purposes. In later stages, these cost items will be presented separately and with details.

Cost plan B

The hospital building design was developed to have 15 beds with an approximate GFA of 3,156 m2.

Documents used

This Stage B cost plan has been prepared using the following documents provided by the relevant consultants:

- architectural drawings (Proposed Schedule of Accommodation/Area Schedule, Site Plan, Floor Plan of the selected concept design)

- engineering drawings (Structural and Civil Sketches)

- geotechnical report

- services engineering feasibility cost estimate (prepared by the engineering services cost consultant of the project)

- structural foundation and fill options analysis.

Basis for measurement and pricing

- The rates included in the cost plan have been generated using the project's cost consulting company's database of historical costs, adjusted for the specific nature of this project (i.e. time, location).

- An elemental basis has started to be used in this stage.

- The rates for engineering services have been provided by the project's services consultants.

- The rates are current at the time as at May 2012 (BPI 190).

Preliminaries and contingencies

- The preliminaries allowance is based on 12% of the total construction costs and is shown separately in the cost plan summary.

- Design contingency allowance is still 5% in this stage as the design risk still pertains.

Project costs

- Project cost items are calculated using similar percentages to Stage A.

- Consultants' fees – The figure provided by the project management company increased to $1.5 million.

Assumptions

- Substructure – The estimate for the substructure is based on the site fill design option provided by the structural engineers

- External Walls – Assumed brick veneer external wall construction with 15% of external wall area as external feature cladding.

- Windows – Assumed 25% of external wall area for aluminium framed windows.

- External Doors – Assumed 8% of external wall area for external doors.

- Infrastructure – Sewer relocation costs are based on indicative cost estimate provided by the relevant engineering cost consultant.

Exclusions

The following items are expressly excluded from the cost plan:

- project prolongation contingency

- allowance of temporary accommodation for the hospital

- hospital operations costs

- land cost

- Impact of Carbon Tax

- GST.

The following items have been costed, however, they will need to be separately funded (not within the project budget mentioned in Stage A):

- demolition of the existing hospital.

The estimate for the demolition of the existing hospital was only preliminary at this stage.

The following items are assumed to be included elsewhere in the client's overall project budget:

- artworks

- client finance costs

- client insurances

- client legal costs

- client marketing costs

- models/visuals.

Risks and opportunities

The following items present the most significant costs risks to the project given the current stage of the design:

- risk of further increases to GFA due to changing project requirements

- potential to re-use site silt layer to be verified

- authority charges and fees to be confirmed.

The following items present opportunities to reduce the current cost estimate, which could be explored at later stages in the design:

- reduce cost for imported structural fill based on finding a local supply of suitable quality

- adjustment of current building location to reduce the extent of fill

- adopt the most suitable substructure option as selected for the filled area

- refine Fittings, furniture and Equipment (FF&E) and IT & Communications (ICT) budgets.

Cost plan B summary

Date of Cost plan B: 09 July 2012

Gross Floor Area (GFA): 3,156 m2

| Description | Total | Cost per m2 of GFA | % of TEC |

| Shell | 2,716,424 | 861 | 12.0 |

| Fit-out | 2,761,500 | 875 | 12.1 |

| Services | 3,695,676 | 1,171 | 16.3 |

| Subtotal – Building Costs | 9,173,600 | 2,907 | 40.4 |

| Project Specifics | |||

| Centralised Energy and Infrastructure Services | 2,606,130 | 826 | 11.5 |

| External Works and External Services | 2,317,176 | 734 | 10.2 |

| ESD Initiatives | 262,000 | 83 | 1.2 |

| Flood Resilience Works | 369,900 | 117 | 1.6 |

| Subtotal | 14,728,806 | 4,667 | 64.9 |

| Preliminaries @ 12% | 1,767,457 | 560 | 7.8 |

| Net Construction Costs | 16,496,263 | 5,227 | 72.7 |

| Contingencies | |||

| Design Contingency @ 5% | 824,813 | 261 | 3.6 |

| Construction Contingency @ 5% | 824,813 | 261 | 3.6 |

| Total Current Construction Cost | 18,145,889 | 5,750 | 79.9 |

| Escalation to construction commencement - Apr 2013 @ 0.50% | 90,729 | 29 | 0.4 |

| Escalation to construction completion - Oct 2014 @ 1% | 181,459 | 57 | 0.8 |

| Total Estimated Construction Cost (TCC) | 18,418,077 | 5,836 | 81.1 |

| Other Project Costs | |||

| Fittings, Furniture and Equipment (FF&E) @ 8% | 1,473,446 | 467 | 6.5 |

| ICT @ 5% | 920,904 | 292 | 4.1 |

| Consultant fees | 1,500,000 | 475 | 6.6 |

| Authority charges, headworks fees, etc. @ 0.6% | 110,508 | 35 | 0.5 |

| Agency management support/administration @ 0.75% | 138,136 | 44 | 0.6 |

| DH management support/administration @ 0.75% | 138,136 | 44 | 0.6 |

| Total Estimated End Cost (TEC) | 22,699,207 | 7,192 | 100.0 |

Total End Project Cost is expressed as 22,700,000.

| Description | Total | Cost per m2 of GFA | % |

| Shell | |||

| Substructure | 801,624 | 254 | 29.5 |

| Columns | 157,800 | 50 | 5.8 |

| Upper Floors | 78,900 | 25 | 2.9 |

| Staircases | - | - | - |

| Roof | 946,800 | 300 | 34.9 |

| External Walls | 613,900 | 195 | 22.6 |

| Windows | 89,000 | 28 | 3.3 |

| External Doors | 28,400 | 9 | 1.0 |

| Subtotal - Shell | 2,716,424 | 861 | 100 |

| Fit-out | |||

| Internal Walls | 261,948 | 83 | 9.5 |

| Internal Screens | 88,368 | 28 | 3.2 |

| Internal Doors | 233,544 | 74 | 8.5 |

| Wall Finishes | 631,200 | 200 | 22.9 |

| Floor Finishes | 394,500 | 125 | 14.3 |

| Ceiling Finishes | 347,160 | 110 | 12.6 |

| Fitments | 678,540 | 215 | 24.6 |

| Special Equipment | 126,240 | 215 | 4.6 |

| Subtotal - Fit-out | 2,761,500 | 875 | 100 |

| Services |

|||

| Sanitary Fixtures | 410,280 | 130 | 11.1 |

| Sanitary Plumbing | 410,280 | 130 | 11.1 |

| Water Supply | - | - | - |

| Gas Service | - | - | - |

| Space Heating | - | - | - |

| Ventilation | - | - | - |

| Evaporative Cooling | - | - | - |

| Air Conditioning | 1,192,968 | 378 | 32.3 |

| Fire Protection | 233,544 | 74 | 6.3 |

| Electric Light & Power | 959,424 | 304 | 26.0 |

| Communications | 331,380 | 105 | 9.0 |

| Transport Systems | - | - | - |

| Special Systems | 157,800 | 50 | 4.3 |

| Subtotal - Services | 3,695,676 | 1,171 | 100.0 |

Reconciliation to Previous Cost Plan

| Description | Total $ |

| Current Cost Plan (Cost plan B) | 22,700,000 |

| Previous Cost Plan (Cost plan A) | 22,700,000 |

| The increase from previous cost plan | NIL |

Budget Reconciliation

| Description | Total $ |

| Current approved budget for the project | 22,700,000 |

| Current estimated total end cost (as per Cost plan B) | 22,700,000 |

There is no anticipated surplus or shortfall to currently approved funding.

Learnings from sample Cost plan B of the hospital project

Basis of the cost plan: This Stage B cost plan is prepared based on the selected outline proposal. GFA is available. Stage A cost plan was based on functional areas of the building, where this Stage B cost plan includes elemental breakdown of costs.

Elemental Breakdown: The cost plan summary presents the building cost under categories, namely shell, fit-out and services. However, this cost plan is prepared using an elemental breakdown. Elemental breakdowns of Centralised Energy and Infrastructure Services, External Works and External Services are also available.

Preliminaries are now added as a percentage (12%) to the Net Construction Cost; whereas, preliminaries for building works were captured in benchmark rates in the Stage A cost plan.

Calculation of Escalation: It is interesting to note that in the Stage A cost plan, Escalation is applied at the end before calculating the other project costs. However, in this cost plan, escalation is applied at the Total Construction Cost before calculating the other project cost allowances. If you do a simple calculation, this order makes no difference when applying percentages. However, the consultancy fees are a fixed amount and should be calculated at current rates.

Cost plan C

From Stage B to Stage C, the design is further refined, and the GFA is now 3,148 m2, whereas it was 3,156 m2 previously.

Additional Department of Health funding of $452,958 is now approved.

Scope of work

The project now includes the following:

- demolition of the old hospital

- cost of all land purchases

- all initial consultants fees engaged by the client.

Basis for measurement and pricing

- Elemental cost planning is used in this stage.

- The rates were current at the time of Sep 2012 (BPI 195).

- ESD design allowance is now fixed at $ 175,000.

Special Provisions

- Escalation %

- Design contingency allowance is now 3% in this stage (within the Department of Health Guidelines).

Other project costs

The cost estimate includes the following costs in accordance with project requirements:

- purchase of the original land $299,990 (expended)

- initial consultancy fees $127,887 (expended)

- demolition of the old hospital $320,000 (estimated).

The estimate for the demolition of the existing hospital was only preliminary at this stage. This estimate was tested in the marketplace in the later few weeks.

Preliminaries

- The preliminaries allowance is now calculated at 11% of the total construction costs as appropriate to the project scope.

Assumptions

- Substructure – The estimate for the substructure is based on the site fill design option provided by the structural engineers and assumes locally sourced material to be used for site fill.

- Infrastructure – Sewer relocation costs are based on indicative cost estimates provided by the relevant engineering cost consultant.

- Other assumptions made in the previous stage are no longer required as the design is now further developed.

Remember interim cost plans may be prepared in this stage (see Section 7.2.1)

This project has an interim cost plan and, therefore, these are named as cost plan C1 and C2.

Cost plan C1 summary

Date of Cost plan C1: 22 October 2012

GFA: 3,148 m2

| Description | Total | Cost per m2 of GFA | % of TEC |

| Shell | 3,180,284 | 1,010 | 13.7 |

| Fit-out | 2,890,558 | 918 | 12.5 |

| Services | 3,785,103 | 1,202 | 16.3 |

| Subtotal – Building Costs | 9,855,945 | 3,131 | 42.5 |

| Project Specifics | |||

| Centralised Energy and Infrastructure Services | 2,461,700 | 782 | 10.6 |

| External Works and External Services | 2,334,090 | 741 | 10.1 |

| ESD Initiatives | 175,000 | 56 | 0.8 |

| Flood Resilience Works | 404,040 | 1.7 | |

| Subtotal | 15,230,775 | 4,838 | 65.6 |

| Preliminaries @ 11% | 1,675,385 | 532 | 7.2 |

| Net Construction Costs | 16,906,160 | 5,370 | 72.9 |

| Contingencies | |||

| Design Contingency @ 3% | 507,185 | 161 | 2.2 |

| Construction Contingency @ 5% | 845,308 | 269 | 3.6 |

| Total Current Construction Cost | 18,258,653 | 5,800 | 78.7 |

| Escalation to construction commencement - Apr 2013 @ 0.25% | 45,647 | 15 | 0.2 |

| Escalation to construction completion | 155,210 | 49 | 0.7 |

| Total Estimated Construction Cost (TCC) | 18,459,509 | 5,864 | 79.6 |

| Other Project Costs | |||

| Fittings, Furniture and Equipment @ 7% | 1,292,166 | 410 | 5.6 |

| ICT @ 3.5% | 646,083 | 205 | 2.8 |

| Consultant fees | 1,550,000 | 492 | 6.7 |

| Authority charges, headworks fees, etc. @ 0.5% | 92,298 | 29 | 0.4 |

| Agency management support/administration @ 0.75% | 138,446 | 44 | 0.6 |

| DH management support/administration @ 0.75% | 138,446 | 44 | 0.6 |

| Allowance for Sewer Diversion Works | 135,200 | 43 | 0.6 |

| Original Land Purchase | 249,990 | 79 | 1.1 |

| Additional Land Purchase | 50,000 | 16 | 0.2 |

| Demolition of Old Hospital | 320,000 | 102 | 1.4 |

| Initial Planning and Business Case Cost | 127,887 | 41 | 0.6 |

| Total Estimated End Cost (TEC) | 23,200,025 | 7,370 | 100.0 |

Extracts of Elemental breakdowns for Shell, Fit-out and Services

| Description | Total | Cost per m2 of GFA | % | |

| Shell | ||||

| 01 SB | Substructure | 820,864 | 260 | 25.8 |

| 02 CL | Columns | 73,101 | 23 | 2.3 |

| 03 UF | Upper Floors | - | - | - |

| 04 SC | Staircases | - | - | - |

| 05 RF | Roof | 1,301,847 | 412 | 40.9 |

| 06 EW | External Walls | 638,072 | 202 | 20.1 |

| 07 WW | Windows | 180,400 | 57 | 5.7 |

| 08 ED | External Doors | 166,000 | 53 | 5.2 |

| Subtotal – Shell | 3,180,284 | 1,008 | 100.0 | |

| Fit-out | ||||

| 09 NW | Internal Walls | 203,593 | 65 | 7.0 |

| 10 NS | Internal Screens | 210,945 | 67 | 7.3 |

| 11 ND | Internal Doors | 355,950 | 113 | 12.3 |

| 12 WF | Wall Finishes | 751,707 | 238 | 26.0 |

| 13 FF | Floor Finishes | 394,595 | 125 | 13.7 |

| 14 CF | Ceiling Finishes | 420,245 | 133 | 14.5 |

| 15 FT | Fitments | 491,573 | 156 | 17.0 |

| 16 SF | Special Equipment | 61,950 | 20 | 2.1 |

| Subtotal - Fit-out | 2,890,558 | 916 | 100.0 | |

| Services | ||||

| 17 SF | Sanitary Fixtures | 883,827 | 280 | 23.4 |

| 18 PD | Sanitary Plumbing | - | - | - |

| 19 WS | Water Supply | - | - | - |

| 20 GS | Gas Service | - | - | - |

| 21 SH | Space Heating | - | - | - |

| 22 VE | Ventilation | - | - | - |

| 23 EC | Evaporative Cooling | - | - | - |

| 24 AC | Air Conditioning | 1,206,198 | 382 | 31.9 |

| 25 FP | Fire Protection | 231,378 | 73 | 6.1 |

| 26 LP | Electric Light & Power | 967,890 | 307 | 25.6 |

| 27 CM | Communications | 330,540 | 105 | 8.7 |

| 28 TS | Transport Systems | - | - | - |

| 29 SS | Special Systems | 165,270 | 52 | 4.4 |

| Subtotal – Services | 3,785,103 | 1,199 | 100.0 |

Extract of detailed item-wise cost breakdown for Substructure

| Item | Description |

Quantity | Unit | Rate | Total |

| 01 | Substructure | ||||

| Ground Slab | |||||

| A | 100 thick concrete slab. SL82 mesh top, 30mm cover on 0.2mm moisture barrier on 50mm compacted sand bed | 3,284 | m2 | 155 | 509,020 |

| B | Termite Barrier | 557 | m | 22 | 12,254 |

| C | Allow for setdowns to wet area | 257 | m2 | 60 | 15,420 |

| Pad Footings | |||||

| D | Pad Footing 300 x 500 X 1600D (PF1) | 2 | m3 | 600 | 1,200 |

| E | Pad Footing 1200 x 1200 X 600D (PF2) | 3 | m3 | 600 | 1,800 |

| F | Pad Footing 900 x 900 X 600D (PF3) | 6 | m3 | 600 | 3,600 |

| G | Pad Footing 450 dia X 600D (PF4) | 2 | m3 | 600 | 1,200 |

| Strip Footing | |||||

| H | Strip footing 500 x 500D [SF500] | 2 | m3 | 700 | 1,400 |

| I | Strip Footing 500 D [SFA, SFB] | 2 | m3 | 700 | 1,400 |

| Edge Beams/Internal Beams | |||||

| J | Edge Beam 300W x 500D (EB300) | 116 | m3 | 700 | 81,200 |

| K | Internal Beam 300W x 500D (IB300) | 192 | m3 | 700 | 134,400 |

| Sundries | |||||

| L | Miscellaneous connections (5%) | 38,145 | |||

| M | Allowance for 500mm high precast perimeter upstand beam along external walls | 305 | m2 | 65 | 19,825 |

| Total – Substructure | 820,864 |

Reconciliation to Previous Cost Plan

| Description | Total $ |

| Current Cost Plan (Cost plan C1) | 23,202,025 |

| Previous Cost Plan (Cost plan B) | 22,700,000 |

| The increase from previous cost plan | 502,025 |

The reason for this increase is the inclusion of the following scope into the cost plan:

- demolition of the existing hospital

- land purchase and

- initial consultant fees.

Budget Reconciliation

| Description | Total $ |

| Approved Project Funding | 22,700,000 |

| Additional Department of Health Funding | 452,958 |

| Total Available Funding (Budget) | 23,152,958 |

| Current estimated total end cost (as per Cost plan C1) | 23,202,025 |

| Shortfall to current funding | 49,067 |

An interim cost plan (Cost plan C2) had to be prepared due to this shortfall.

Interim Cost plan C2 summary

The design is further refined and the GFA is now 3,181 m2, whereas it was 3,148 m2 previously.

Date of Cost plan C2: 13 January 2013

GFA: 3,181 m2

| No. | Description | Total | Group total | Cost/m2 of GFA | % |

| Shell | 3,206,000 | 1,007.86 | 28.70 | ||

| 01 SB | Substructure | 826,000 | 259.67 | 7.4 | |

| 02 CL | Columns | 73,000 | 22.95 | 0.7 | |

| 03 UF | Upper Floors | - | - | - | |

| 04 SC | Staircases | - | - | - | |

| 05 RF | Roof | 1,206,000 | 379.13 | 10.8 | |

| 06 EW | External Walls | 721,000 | 226.66 | 6.5 | |

| 07 WW | Windows | 244,000 | 76.71 | 2.2 | |

| 08 ED | External Doors | 136,000 | 42.75 | 1.2 | |

| Fit-out | 2,928,000 | 920.47 | 26.2 | ||

| 09 NW | Internal Walls | 216,000 | 67.90 | 1.9 | |

| 10 NS | Internal Screens | 149,000 | 46.84 | 1.3 | |

| 11 ND | Internal Doors | 352,000 | 110.66 | 3.2 | |

| 12 WF | Wall Finishes | 815,000 | 256.21 | 7.3 | |

| 13 FF | Floor Finishes | 397,000 | 124.80 | 3.6 | |

| 14 CF | Ceiling Finishes | 440,000 | 138.32 | 3.9 | |

| 15 FT | Fitments | 505,000 | 158.76 | 4.5 | |

| 16 SE | Special Equipment | 54,000 | 16.98 | 0.5 | |

| Building Services | 3,931,000 | 1,235.77 | 35.2 | ||

| 17 SF | Sanitary Fixtures | 1,064,000 | 334.49 | 9.5 | |

| 18 PD | Sanitary Plumbing | - | - | - | |

| 19 WS | Water Supply | - | - | - | |

| 20 GS | Gas Service | - | - | - | |

| 21 SH | Space Heating | - | - | - | |

| 22 VE | Ventilation | - | - | - | |

| 23 EC | Evaporative Cooling | - | - | - | |

| 24 AC | Air Conditioning | 1,332,000 | 418.74 | 11.9 | |

| 25 FP | Fire Protection | 279,000 | 87.71 | 2.5 | |

| 26 LP | Electric Light & Power | 753,000 | 236.72 | 6.7 | |

| 27 CM | Communications | 239,000 | 75.13 | 2.1 | |

| 28 TS | Transport Systems | - | - | - | |

| 29 SS | Special Systems | 264,000 | 82.99 | 2.4 | |

| Subtotal | 10,065,000 | 3,164 | 90.1 | ||

| 00 PR | Preliminaries (Proportion for Elements 01 to 29) at 11% | 1,107,000 | 348 | 9.9 | |

| Total Building Cost | 11,172,000 | 3,512 | 100.0 | ||

| 30 CE | Centralised Energy Systems | 2,377,000 | |||

| 31 AR | Alterations & Renovations | - | |||

| Site Works | 2,816,000 | 885.26 | |||

| 32 XP | Site Preparation | 948,000 | 298.02 | 0.05 | |

| 33 XR | Roads, Footpaths and Paved Areas | 942,000 | 296.13 | 0.05 | |

| 34 XN | Boundary Walls, Fencing and Gates | 85,000 | 26.72 | 0.00 | |

| 35 XB | Outbuildings and Covered Ways | 587,000 | 184.53 | 0.03 | |

| 36 XL | Landscaping and Improvements | 254,000 | 79.85 | 0.01 | |

| External Services | 515,000 | 161.90 | |||

| 37 XK | External Storm Water Drainage | 515,000 | 161.90 | ||

| 38 XD | External Sewer Drainage | Included | |||

| 39 XW | External Water Supply | Included | |||

| 40 XG | External Gas | Included | |||

| 41 XF | External Fire Protection | Included | |||

| 42 XE | External Electric Light and Power | Included | |||

| 43 XC | External Communications | Included | |||

| 44 XS | External Special Services | - | |||

| ESD Allowance (Fixed) | Included | ||||

| 45 XX | External Alterations & Renovations | - | |||

| 00 PR | Preliminaries (Proportion for Elements 30 to 45) at 11% | 628,000 | 197 | ||

| Net Construction Cost | 17,508,000 | 5,503.93 | |||

| 46 YY | Special Provisions | 1,138,000 | 357.75 | ||

| Infrastructure Upgrade Allowance [Included in Centralised Energy Systems] | Included | ||||

| Design Contingency (1.5%) | 262,600 | ||||

| Construction Contingency (5%) | 875,400 | ||||

| Total Construction Cost | 18,646,000 | 5,861.68 | |||

| Other Project Costs | 4,307,000 | 1,353.98 | |||

| Fittings, Furniture and Equipment | Fixed | 1,175,216 | |||

| IT & Communications & Audiovisual Equipment | Fixed | 446,129 | |||

| Consultant Fees | Fixed | 1,550,000 | |||

| Authority Charges, Headwork Fees, etc. | Fixed | 60,000 | |||

| Agency Management Support/Administration | Fixed | 138,456 | |||

| DH Management Support/Administration | Fixed | 138,456 | |||

| Allowance for Sewer Diversion Works | Fixed | 116,000 | |||

| Original Land Purchase | Fixed | 249,990 | |||

| Additional Land Purchase | Fixed | 25,000 | |||

| Demolition of Old Hospital | Fixed | 280,000 | |||

| Initial Planning and Business Case Cost | Fixed | 127,887 | |||

| Total Current Project Cost (as at Nov 2012) | 22,953,000 | 7,215.66 | |||

| Escalation (On Total Construction Cost) | 200,000 | 62.87 | |||

| Total Project End Cost (excluding Goods and Services Tax) | 23,153,000 | 7,278.53 |

Extract of detailed item-wise cost breakdown for Substructure

| No. | Description | Quantity | Unit | Rate | Total |

| 01 | Substructure | ||||

| Ground Slab | |||||

| 1.1 | 100 thick concrete slab. SL82 mesh top, 30mm cover on 0.2mm moisture barrier on 50mm compacted sand bed | 3,330 | m2 | 155 | 516,150 |

| 1.2 | Extra over for 150 thick ground slab | 67 | m2 | 55 | 3,685 |

| 1.3 | Termite Barrier | 700 | m | 22 | 15,400 |

| 1.4 | Allow for setdowns to wet area | 259 | m2 | 60 | 15,540 |

| Pad Footings | |||||

| 1.5 | Pad Footing 300 x 500 X 1600D (PF1) | 2 | m3 | 600 | 1,200 |

| 1.6 | Pad Footing 1200 x 1200 X 600D (PF2) | 4 | m3 | 600 | 2,400 |

| 1.7 | Pad Footing 900 x 900 X 600D (PF3) | 8 | m3 | 600 | 4,800 |

| 1.8 | Pad Footing 450 dia X 600D (PF4) | 3 | m3 | 600 | 1,800 |

| Strip Footing | |||||

| 1.9 | Strip footing 500 x 500D [SF500] | 2 | m3 | 700 | 1,400 |

| 1.10 | Strip Footing 500 D [SFA, SFB] | 8 | m3 | 700 | 5,600 |

| 1.11 | Strip footing 300 x 500 [SF300] | 2 | m3 | 700 | 1,400 |

| Edge Beams/Internal Beams | |||||

| 1.12 | Edge Beam 300W x 500D (EB300) | 110 | m3 | 700 | 77,000 |

| 1.13 | Internal Beam 300W x 500D (IB300) | 180 | m3 | 700 | 126,000 |

| Sundries | |||||

| 1.14 | Miscellaneous connections - 5% | 38,619 | |||

| 1.15 | Allowance for 500mm high precast perimeter upstand beam along external walls | 150 | m2 | 100 | 15,000 |

| Total | 825,994 |

Reconciliation to Previous Cost Plan

| Description | Total $ |

| Current Cost Plan (Cost plan C2) | 23,153,000 |

| Previous Cost Plan (Cost plan C1) | 23,202,000 |

| The decrease from the previous cost plan | 49,000 |

There were value management exercises carried out resulting in savings from the previous cost plan C1.

Budget Reconciliation

| Description | Total $ |

| Total Approved Budget | 23,152,958 |

| Current estimated total end cost (as per Cost plan C2) | 23,153,000 |

| Shortfall to current funding | 41.77 |

Learnings from sample Cost plan C of the hospital project

- Interim cost plans are required if the estimated project cost exceeds the approved budget. This usually happens between Stages C and D because in Stage D, the tender document cost plan will be prepared with finalised details.

- Design contingency allowance was initially reduced to 3% from Stage B, and further into 1.5% in the cost plan C2 as the design has been further developed now that more detailed information is available. Hence, the design risk is now low and the design contingency allowance has been reduced.

Cost plan D

This is the Documentation Stage and the Tender Document Cost Plan is prepared in this stage marking the final stage of the cost planning process.

Basis of measurement of works and pricing

- Trade-wise costing is done in this stage.

- Net Construction Cost has been calculated with more detailed costing of work items with current rates at the time. Therefore, escalation allowance is not separately presented and captured within the construction cost.

- Preliminaries are now calculated in detail with current rates instead of allocating a percentage, and included in the Net Construction Cost.

Special Provisions

- Design contingency allowance is now 0% because the design is finalised at this stage.

- Contract contingency allowance remains through to the construction stage.

Date of Cost plan D: 28 February 2013

GFA: 3,181 m2

| Element Group | Cost per GFA ($/m2) | Total |

| Net Construction Cost | 5,637 | 17,932,400 |

| Special Provisions | ||

| Design Contingency (0%) | 0 | |

| Construction Contingency (5%) | 896,620 | |

| Total Current Construction Cost | 5,919 | 18,829,020 |

| Escalation | Included | |

| Total Estimated Current Construction Cost (TCC) | 5,919 | 18,829,020 |

| Other Project Costs (Fixed) | ||

| Furniture & Equipment | 1,155,216 | |

| IT & Communications & Audiovisual Equipment | 446,129 | |

| Consultant Fees | 1,557,000 | |

| Authority Charges, Headwork Fees, etc. | 90,000 | |

| Agency Management Support/Administration | 138,456 | |

| DH Management Support/Administration | 138,456 | |

| Allowance for Sewer Diversion Works | 116,000 | |

| Original Land Purchase | 249,990 | |

| Additional Land Purchase | 25,000 | |

| Demolition of Old Hospital | 280,000 | |

| Initial Planning and Business Case Cost | 127,887 | |

| Total Project Cost - Current (at Feb 2013) | 7,279 | 23,153,154 |

| Total Project End Cost (excluding GST) (Rounded) | 7,279 | 23,153,000 |

7.2 Cost planning process in the New Zealand context

The New Zealand Construction Industry Council (NZCIC) Design Guidelines provide the stages in a construction project and the Elemental Analysis of Costs of Building Projects (NZIQS, 2017) is used for cost management exercises, following its elemental breakdown, definitions and measurement rules. This section provides insights into the cost planning process of construction projects in New Zealand.

7.2.1 Project establishment stage

At this stage, the project will be started and established. The client or the consultants will start collecting preliminary information regarding the site, time frame, budget and stakeholders. Client’s brief information will be created at this stage, which should help manage the rest of the project stages. Factors that impact the consultant’s scope and program like the procurement process will be established at this stage.

Costing

No estimate will be prepared at this stage. Only the client's budget restrictions will be identified.

7.2.2 Concept design stage

At this stage, different design concepts are explored to check if the client’s brief is achievable. In this sense, the site is checked to see if the project can be developed there and the concept estimate is prepared to check the feasibility of the project. To go forward from design to resource consent, the required consultants are engaged in this process. An outline of the legal constraints and compliance is also accumulated. When the client approves the concept design, program and initial estimate, the next stage can begin.

In some projects, a single stage will cover project establishment and concept design.

Cost

- Concept cost estimates will be prepared for each concept design to check the project’s feasibility.

Costing process

- Cost planners typically use the functional area method or functional unit method (see Chapter 3) to estimate the project cost.

- Historical cost data will be used for costing and then adjusted based on the location, building type, price and date (see Chapter 4).

Industry insights

- Similar to that of the Australian context, the functional area method is preferred in this stage.

- Historical data from comparative past projects, QV Cost Builder database and market insight updates from Rider Levett Bucknall (RLB) are used as data sources to develop the unit rates. Some companies maintain their own database for this purpose (see Chapter 4).

7.2.3 Preliminary design stage

The concept design was further developed at this stage into the preliminary design. The preliminary design would include a scale, spatial sizes, cross-section drawings, elevation drawings, major structural elements zones and plant rooms. This includes selecting major elements such as building material, structure type and mechanical process. These selections and designs should be compatible with governmental regulations, resource consent and building consent requirements. Specialised consultants will be selected and hired at this stage to develop Resource Consent.

Resource Consent involves obtaining approval from the local council for activities that have an impact on the environment (Ministry for the Environment, 2021).

Based on the updated design and details, the project program and estimate will be updated. At this stage, preliminary estimates are developed to check project feasibility. At the end of this stage, Resource Consent might be applied.

Cost

- Preliminary cost estimates will be prepared for each concept design to check the project’s feasibility.

Costing process

- Cost estimators typically use the Elemental Analysis of Costs of Building Projects (NZIQS, 2017) to estimate the project cost. Based on the available details, QS practitioners will decide detailed depth of the estimation process.

- Historical data are used for elemental costs and should be adjusted based on the location, building type, price, date and construction element type variations.

Industry insights

- In addition to published data sources, instance quotations from builders are sometimes used as data sources to develop the unit rates. This depends on access to such quotations in the network as contractors/builders sometimes are not willing to provide quotations for these estimates.

7.2.4 Developed design stage

A developed design will be completed at this stage so the client and relevant stakeholders can approve the aesthetics, functionality and cost of the project. The design should clearly define and coordinate major building elements and gross building areas. The scope of all building elements is finalised so that there are only a few missing details. Design documentation with scales, levels, and dimensions will be produced. All parties must work together to complete this stage.

In some projects, this stage is combined with the preliminary design stage so that there will be one estimate developed.

Cost

- An elemental cost plan is developed.

Costing process

- Similar to the preliminary stage, the Elemental Analysis of Costs of Building Projects (NZIQS) can be used to estimate the project cost or previous estimates are updated at this stage.

7.2.5 Detailed design stage

At this stage, a detailed design will be developed to have clear and defined quality and quantity of all building systems, elements and materials. Design professionals from all disciplines work together and coordinate to develop a detailed design which should include drawings, specifications, schedules and performance requirements. These details designs will be used to apply for building consent which should include tender document details. Cost planners develop a tender estimate to evaluate the contractor’s tender submissions which might be a Schedule of Quantities.

Cost

- Preparation of tender document.

- Consultant’s Schedule of Quantities for tender evaluation is developed based on detailed design.

Costing process for tender document preparation

- The Elemental Analysis of Costs of Building Projects (NZIQS, 2017) or ANZSMM (AIQS et al., 2022) is used to develop the cost estimate. Specific documents used depend upon the consultant's and client's requirements.

- The consultant will develop their own BOQ or SOQ to evaluate the tender document.

- If the ANZSMM is used, NZIQS has developed a sample BOQ/SOQ which might be used by QS to develop the estimate and the BOQ/SOQ can be included in the tender document.

7.2.6 Procurement stage

In this stage, the cost planning process is concluded, and the final contract price is agreed with the selected builder.