Chapter 6: Cost Planning Construction Projects

6.0 Introduction

Cost is a key aspect of a construction project, and cost management is a process that is carried out throughout various stages of a construction project. Chapter 2 (Table 2.1) presented the cost management stages of a construction project as specified in the standard documents in several contexts, including Australia, New Zealand and the United Kingdom. The pre-construction cost management phase involves design development and cost planning processes, which are usually carried out simultaneously until the tender documentation. However, there can be changes based on the selected procurement method, and consultancy firms might follow this process with slight differences. This chapter focuses on the fundamentals of cost planning construction projects, including the basis of a cost plan, and concludes with the elaboration of major cost items in a cost plan.

6.1 Cost plan

The cost of a construction project is derived by pricing all relevant components of a project. A cost plan is a descriptive statement that shows the proposed distribution of the budget through the elements or sub-elements of the project. In this way, cost plans provide design parameters and cost targets for the design development within the project budget. Therefore, cost plans involve a process rather than a one-off estimate, and this process helps to give the client value for money by achieving a good balance of expenditure between the various components of the building project. A range of information is required in these pricing exercises at various stages.

Cost planning is carried out by using available project details combined with various other documents prepared by different players in a construction project. As the design develops, these documents will be updated with the latest information, and cost plans will also be updated with an increased level of project information. Historical data with adjustments based on sensitive factors like time, quality and location is a key ingredient in a cost plan (see Chapter 4).

A cost estimate and a cost plan should not be confused.

Note: Chapter 1 discussed the different parties to a construction contract and various professionals involved in a construction project. This section refers to the client, cost planner, quantity surveyor, cost consultants, contractor and estimator.

- When costing is carried out by the contractor’s estimator for bidding purposes, we call it a contractor's/builder's estimate.

- When costing is carried out by the client’s representative (cost consultants, cost planner, quantity surveyor) for cost management purposes in the pre-construction phase, we call it a cost plan.

- A cost plan will be updated with the design development. This involves designing to a cost (i.e. budget).

- The term estimate is used for a one-time figure at different points in the cost planning process.

- Therefore, the terms 'estimating' and 'estimates' are used in this book throughout the cost planning process.

Bills of Quantities (BQ) is also a key document used for cost managing construction projects. It's important to differentiate these terms. Table 6.1 compares the characteristics of cost plan and BQ.

| Cost plan | Bills of quantities |

|---|---|

| Involves a process and update alongside the design development stages during the pre-construction cost management phase. | Prepared at the tender document stage for tendering purposes and used for contract administration in later stages of cost management. |

| Prepared from early stage information through to the near completion of documentation. | Prepared with detailed measurements when sufficient information is available. |

| Prepared in elements as per Australian Cost Management Manuals and NZIQS Elemental Cost Analysis. (NZIQS, 2017) e.g. Substructure, External Walls, Roof, Windows |

Prepared in trades, measured as per Australian and New Zealand Standard Method of Measurement (ANZSMM) (AIQS et al., 2022). e.g. Masonry, Concrete, Painting *One element contains several trades e.g. External Walls includes Masonry, Insulation and Painting |

| Provides other project costs as well, thus creates a wholistic view of the total end project cost to the client. These other costs can include demolition costs, land costs, professional and legal fees, authority fees and sometimes operational costs and life cycle costs. |

Generally provides only the total construction cost. |

| Not seen by builders. | Sent unpriced BQ to builders for preparing tenders. |

| Priced by cost planners. | Priced by builders’ estimators. |

Table 6.1: Comparison of cost plan and BQ

6.2 Basis of the cost plan

Cost planning is a process and cost plans are documents prepared to predict the end cost to the client with applicable rates. Cost plans are updated with the design development, and the rates applied should be relevant to the project's current context. Therefore, it is paramount to state the basis of a cost plan, in terms of documents used, rates applied and the standards followed. Stating the inclusions and exclusions is also important to provide the client with a clear picture of the cost prediction. This section discusses what needs to be stated as the basis of a cost plan.

6.2.1 Basis of measurement of works

Available information in terms of drawings, specifications, site reports and other documents provides the basis for costing a project. Due to being an evolving process, cost plans need to be updated with the availability of information with the latest revisions of documents. It is very important to state the list of documents used for preparing a cost plan, including the date each document was produced because there may be several revisions. This can be included as a schedule/table with a list of documents and the date issued/received. This provides the basis for the measurement of building works.

In the early stages of cost planning, when the design information is unavailable, appropriate allowances should be established in close consultation with the design team, and assumptions should be stated. This is common in cost planning building services where allowances are made with the advice of services engineering consultants.

6.2.2 Basis of pricing: Base rates, price indices, allowances

Cost plans are mostly prepared using historical cost data unless the latest rates are available to the cost planner. Therefore, it is necessary to state the basis of those historical cost data with the base date, location and quality of the base project. Price indices or allowances should be used to adjust the historical cost data (see Chapter 4). These details should also be stated clearly as the basis of a cost plan.

6.2.3 With or without tax

In Australia and New Zealand, goods and services tax (GST) is applicable, and any cost presented should state whether it includes or excludes GST. If the amounts are including GST, the percentage should be stated.

6.3 Professional practice and documentation

This section provides several good practices a professional cost consultant may follow during the documentation of any cost advice, including the preparation of cost plans as follows:

- Follow and refer to standards.

- Use clear and concise documentation.

As explained in Section 2.3.1, there are standard documents published by professional bodies in various regions. As professionals, it is always recommended to follow standard documents rather than following ad-hoc methods.

There are several benefits to following standards while documenting cost plans:

- Standards provide a uniform basis that can be understandable and can be easily followed by all those involved in a project. It also facilitates easy updates and an iterative process with progressive information. This is important for cost planning where the cost plan is updated with the design development with progressive design information.

- Standards also contain defined breakdown of items, and therefore, the cost plan will contain only the necessary information, making it concise.

- Another benefit of standards is ease of comparison, which helps using benchmark costs, reconciliation of costs between stages and effective cost controlling.

- Standards aid effective communication between the project team members and other parties as they would be familiar with the standard.

- Standards help maintain accuracy as it helps not to miss important components in a process.

- Therefore, using standards will provide trustworthy estimates (i.e. for banks and other financial bodies for approvals).

In Australia, the ACMM is followed to prepare cost plans. In both Australia and New Zealand, the ANZSMM is followed to prepare BQs or schedules of quantities (SOQ). SOQ is widely used in New Zealand.

In addition to these standard documents, there can be standard guidelines published by state government organisations. In Australia, there are guidelines published for building work and other capital works by various government departments. For major public sector projects, the relevant guidelines should be followed in preparing cost plans based on the type of project, apart from the ACMM.

Example: Standard documents

- In Australia, a healthcare project such as a hospital should follow the standards of the Department of Health, Capital Works Guidelines and Department of Health Project Brief.

- In the state of Victoria (Australia), government school building projects should follow the guidelines of the Victorian School Building Authority (VSBA).

- In New Zealand, Cost Estimating Guideline for Public Sector Health Capital Projects [Word, 1.86MB] was developed for the healthcare sector.

- In public sector civil works, Waka Kotahi NZ Transport Agency has produced a Cost Estimation Manual (SM014) for the development of estimates for capital projects.

6.4 Major cost items

This section explains major cost items in a cost plan in accordance with the templates and definitions provided in the ACMM Volume 1 (AIQS, 2022). The Elemental Analysis of Costs of Building Projects (NZIQS, 2017) covers cost items other than the construction cost under 'other development costs'.

| Element | Cost |

|---|---|

| *Elemental/Functional area costs (including or excluding building services) | $ XXXXX |

| Building Services (related to the building, unless included above) | $ XXXXX |

| Preliminaries (related to the building cost) | $ XXXXX |

| Building Cost | $ XXXXX |

| Project specifics | |

| Alterations | $ XXXXX |

| External Works | $ XXXXX |

| External Services | $ XXXXX |

| Preliminaries (related to construction cost other than building cost) | $ XXXXX |

| Net Project Cost/Construction Cost | $ XXXXX |

| Special provisions | |

| Design Contingencies (%) | $ XXXXX |

| Contract Contingencies (%) | $ XXXXX |

| Escalation | $ XXXXX |

| Loose Furniture, Loose Equipment | $ XXXXX |

| All Costs in Connection with Design, Documentation & Supervision | $ XXXXX |

| Statutory Charges | $ XXXXX |

| Headworks | $ XXXXX |

| Client Costs | $ XXXXX |

| Gross Project Cost (excluding GST) | $ XXXXX |

6.4.1 Building cost

Building cost constitutes a major part of the construction cost of a project. Building cost can be derived through suitable cost planning techniques (see Chapter 3) depending on the availability of information (i.e. based on functional area costs or elemental costs). This includes building services cost and the proportion of preliminaries related to the building.

6.4.2 Project specifics

Project specifics are presented separately in a cost plan. These vary from project to project. For example, if the same building layout is used in 2 projects, despite the similar building areas, external works will depend on the site conditions. The proportion of preliminaries related to these items should also be included.

Project specifics can include, but are not limited to:

- alternations

- external works and services external to the building

- any other cost items specific to the project.

6.4.3 Services costs

Services costs are usually known as 'engineering services costs'. This cost in a project is based on advice from services engineering consults or separately provided by them. Building services costs are presented with building costs, while external services costs are presented with external works.

6.4.4 Preliminaries

In the early stage of cost planning, a percentage of relevant costs are calculated as preliminaries. The percentage is decided as appropriate for the project, taking cognisance of program, the complexity of the work and current market conditions. Ideally, these should be estimated as specific to the project requirements.

6.4.5 Construction cost

ACMM (AIQS, 2022) defines this as the 'Construction Cost' or the 'Net Project Cost'. It constitutes the building cost plus project specifics and the related preliminaries. Construction cost plus special provisions and other client's costs will give the total end project cost to the client. This also reflects the major difference between a tender document cost plan and a priced BQ, where the later does not include other project costs to the client, but what is offered by the contractor to carry out construction works.

6.4.6 Special provisions

Risk management items such as contingencies and escalation are calculated as special provisions. There are also other items which might not be included in the main contract, but will incur in the project, and therefore, should be considered in the client's budget. These are calculated under special provisions.

A list of items that are considered under special provisions can be found in the elemental breakdown given in the ACMM.

Works to utilities off-site: Some projects require diversions or capacity enhancements of public utility mains off-site up to the on-site connections, in accordance with project requirements. Examples include the installation of additional electrical substations, improvements to public access roads, or work related to other utility connections, such as water, sewer and gas.

Loose furniture and equipment: These include furniture and equipment not normally covered by the main construction contract. However, this will be a cost to the client as per project requirements. These are not normally installed before the completion of construction and mostly include furniture and equipment that are not stationary but movable (e.g. mobile equipment). These will depend on the type of project (e.g. hospitals and aged care facilities require special mobile equipment).

Professional fees: This cost covers all the design and documentation consultants such as architects, engineering consultants, surveyors, specialist consultants and quantity surveyors. There can be specialist advisors such as a health advisor on a hospital project involved in the project designing and planning due to its specific requirements. It also includes the cost of any value management studies carried out during the design development and cost planning stages. Project director fees, site supervision charges, and project management fees also need to be calculated into the total project cost.

Statutory charges: Costs incurred due to charges and levies in relation to the project duration from planning and design up until the project inspections need to be calculated in cost planning. These also include authority charges for testing.

6.4.7 Contingencies

The ACMM (AIQS, 2022. p. 4) defines 'contingency as an allowance for risks and unforeseen items which could be encountered generally applied to the 'Net Construction Cost'.

As mentioned in Chapter 1, construction projects are unique, complex and subjected to many external conditions. Also, changes to the scope (variations) throughout a construction project are inevitable. Therefore, risk factors should be considered while planning construction projects in terms of time, cost and other resources.

Risk allowances should be included throughout the cost management of construction projects.

AIQS (2022) considers 4 types of contingency factors in cost management:

- Planning Contingency

- Design Contingency

- Contract (Construction) Contingency

- Project Contingency.

The cost planner includes a suitable provision for contingency allowances depending on the nature of the project using their intuition, past experience and historical data. Contingencies are usually calculated as percentages and can vary given the level of design development on a project.

Some public authority guidelines on building works provide recommended percentages to be used on their projects. These can vary with the project type, complexity and special requirements.

Contingency percentages could go higher on complex projects such as those including major alterations and renovations or 'hi-tech' projects such as advanced laboratories.

Planning contingencies

- Early-stage cost plans involve planning risks. For example, those cost plans are based on approximation of functional areas and there is a risk of not being able to plan and design spatial relationships accurately (i.e. functional areas/circulation areas).

- Sometimes the sketches are also not available in very early stages. Therefore, an allowance can be made to cover this risk.

- However, this risk will disappear along with the design development and usually reduced to zero when the building layouts and dimensioned drawings are available.

Design contingencies

- Cost planning as a process evolving with the design development needs to consider the risk of 'unknowns' in the design, depending on the level of information available.

- An allowance is made as a percentage of the net construction cost to cover this design development risk.

- This amount should be shown separately in the cost plan.

- The design contingency allowance will be gradually reduced over the design development and will be zero at the tender document stage when the design is finalised and ready to tender.

In the initial stages, a higher contingency percentage would be added for the design development changes (in New Zealand, this can go up to 30%).

Example: Contingencies

In the example hospital project in Australia (see Chapter 7), the design contingency allowance has been gradually reduced from 5% to 0% throughout the design development stages.

| *Cost plan | Design contingency allowance |

|---|---|

| Stage A | 5% |

| Stage B | 5% |

| Stage C1 | 3% |

| Stage C2 | 1.5% |

| Stage D | 0% |

*This is as per the cost planning stages in accordance with the ACMM. Chapter 7 explains these stages in detail.

Contract (Construction contingencies)

- Variations are inevitable in construction projects, and unforeseen conditions can be encountered during construction.

- An allowance is made as a percentage of the net construction cost to cover these risks of changing scope of work.

- This is an important risk management component.

- This amount should be shown separately in the cost plan.

- This allowance will be constantly included in all cost planning stages and will not disappear like planning and design contingencies because this it involves the risks during construction.

Example: Construction contingencies

In the example hospital project in Australia, (see Chapter 7), the construction contingency allowance of 5% is applied in all stages of cost plan.

Project contingencies

An allowance may be added to cover delays and/or inflation, major changes required by the client or authorities, fee negotiations, latent conditions and similar.

What's happening in the industry?

Project contingencies or project prolongation contingencies are used to cover overall project delays. Government agencies have specified these contingency percentages applicable to their projects and therefore, specifically applied in government projects.

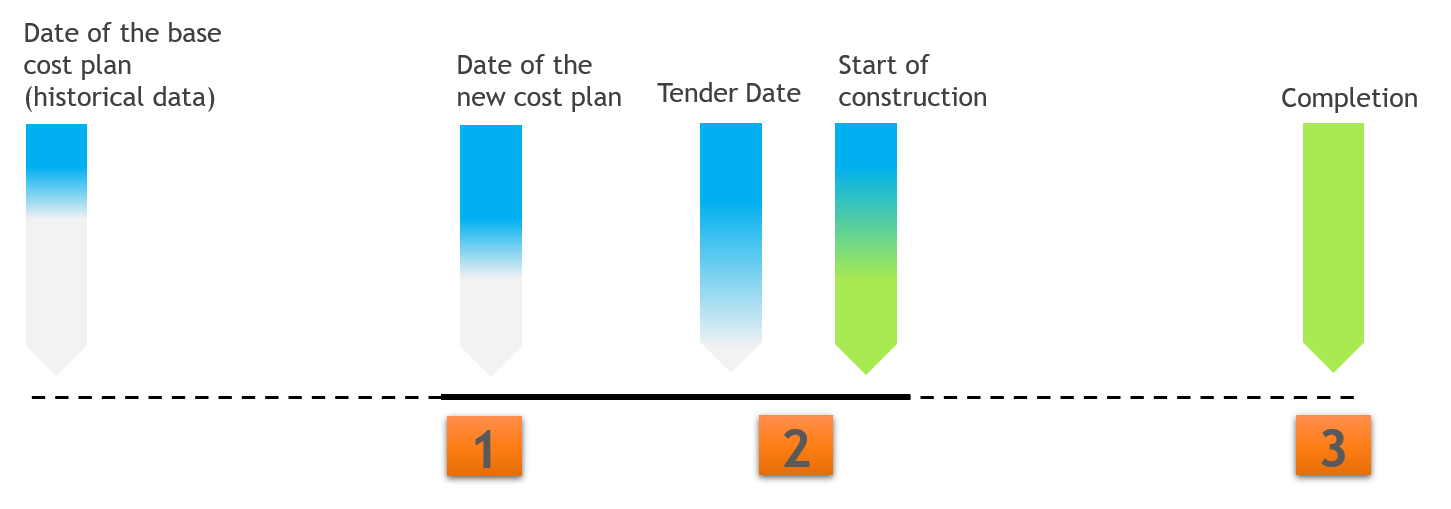

6.4.8 Escalation

Costs associated with construction projects tend to fluctuate over the time. Given the nature of construction projects with longer durations, appropriate escalation factors should be included in cost plans.

Several time periods need to be considered when applying escalation factors.

1. Escalation from the date of base cost plan to the date of the new cost plan

In any cost plan, the prepared date should be stated. If the rates used are applied from a previous project (historical data), they will be adjusted for the time difference. Relevant indices should be used to calculate the escalation and convert those rates into current rates. Chapter 4 and Chapter 5 provide more details about cost data derived by cost analysing previous projects and the use of indices.

2. Escalation from the date of the new cost plan to the tender date/start of construction

There can be a considerable time (several weeks or months) from the date of preparing the cost plan and the tender/start of the construction. Any escalation during this time should be considered as this will affect the prices and cost to the client.

As per cost planners in the industry, the time taken between tender and construction start is generally not very significant. Therefore, the terms 'escalation to tender' or 'escalation to commencement' are used interchangeably in cost plans. Any considerable time periods need be taken into account considering the market conditions.

3. Escalation from the start of construction to project completion

The construction stage can span over months or years. The prices of key project inputs can fluctuate during this project duration. Depending on the procurement method and the payment method (see Section 2.3 for procurement methods), such fluctuations can affect the project cost. It is prudent to include a contractual provision to capture these fluctuations. In Australia, such a clause is usually known as 'rise and fall' and in New Zealand, as 'cost fluctuations'. When there is a contractual provision, major and cost effective items such as cost of steel materials, concrete materials and labour costs will be adjusted using a specified formula. This potential additional cost to the client should be considered and included in cost planning. Cost planners calculate a percentage to apply for this escalation by considering the project's predicted cashflow distribution using project's 'S curve' and market conditions.