Chapter 3: Cost Planning Techniques

3.0 Introduction

Cost planning is carried out in the early stages of the project cost management process, from the very initial brief stage through several design stages until the tender document cost plan. Cost consultants update the cost plans throughout these stages. Therefore, cost planning is not a one-time activity but a process carried out through the pre-construction cost management phase of a project. Various cost planning techniques are used in different stages depending on the level of information available. It is important to identify the suitable cost planning technique for each situation.

3.1 Availability of information

As a project evolves from the early design stages to the construction phase, more design details and other project information become available with the design development. Increasing levels of information facilitate increasing levels of accuracy of cost predictions. Therefore, suitable cost planning techniques should be selected as appropriate to the project stage and the available information.

Before discussing various cost planning techniques, let’s see what type of information affects the cost of a project.

3.1.1 Type of a project/function of a building

There are different types of construction serving various functions. Building types can be classified as residential, commercial, educational, healthcare, industrial, and so on based on those functions. There are specific requirements for each type of project. This helps identify general and specific requirements of a project which incur various costs.

3.1.2 Size of a project

Project size can be indicated by the floor area, number of floors, and also the number of functional units for certain types of projects. For example, a single house does not have a specific functional unit.

3.1.3 Scope/quality of a project

The terms ‘scope’ and ‘quality’ are sometimes used interchangeably. Also, the term ‘quality’ has other broader meanings.

Examples

In this example, the type of project is ‘hotel’, in which the indication of the size of the project comes with 50 guest rooms. It also indicates the quality as ‘3-stars’.

Star categories indicate different levels of services provided in hotels and thus the quality of buildings and facilities. A 5-star hotel certainly incurs higher costs than a 3-star hotel the same size or accommodating the same number of guest rooms.

The scope should be stated clearly with inclusions and exclusions because any changes to the scope can result in a significant change to the cost, and also misunderstandings can occur by overlooking the cost items.

In this example, the cost consultant states the exclusions. Therefore, the client knows that the cost of solar panels is excluded from the current budget and can have a clear understanding of his financial commitments. Having solar panels can also be considered as an indication of the overall quality of the development.

3.2 Cost planning techniques

Cost planning is usually carried out by breaking down the components of a building/project and pricing them to derive the total cost. This is again based on the cost planning stage and the available information. You can find various cost planning techniques and categorisations in other books. This book will discuss the most common techniques followed in Australia and New Zealand. Cost planning techniques can be broadly classified as budget-setting techniques (in the early design stages to set the budget) and budget-distributing techniques (with detailed designs).

Budget-setting techniques:

- functional unit method

- area method

- functional area method.

Budget-distributing techniques:

- elemental cost planning.

3.2.1 Functional unit method

Scenario

Before discussing cost planning construction projects, let’s take a simple example from our daily activities.

Scenario: Imagine that you are asked to organise a morning tea for classmates. You expect 20 attendees, and the budget is $500. You wish to cater cupcakes, mini pizzas and fruit juice bottles. You know that some cafes offer discounts, but you prefer some other cafes due to the quality and taste of food. How do you find out whether you can manage this budget?

Tip: First, as you know the budget and number of attendees, you can calculate the cost per person. We called this a ‘per head cost‘. Then you can check if your menu is affordable or otherwise make any changes easily by checking the available food prices.

‘Per head cost’ in this example is a ‘unit cost’. This can also be applied in cost planning construction projects, in which the functional unit is definable.

Functional unit: Definition

‘… the units of performance or occupancy for which a building or section of a building is functionally designed’ (AIQS 2022, p. 7).

Functional unit is ‘a unit of measurement used to represent the prime use of a building or part of a building’ (RICS 2021b, p. 25).

This rate method is simple and faster. Since this method does not go into specific details, it will have a lot of limitations in its accuracy. This technique is more appropriate for public projects such as hospitals and schools where a functional unit can be identified.

Examples of functional units are:

- hotel – number of rooms

- car park – parking spaces

- hospital – number of beds

- school – number of students.

It is not meaningful to use in projects where a functional unit cannot be indicated to appropriate the size of the building such as a house (a house for 2 adults and 3 kids does not provide a meaningful functional unit. Size indication of 2-bedroom or 3-bedroom house is not necessarily a functional unit compared to the small size of the building and other functional areas, which are not necessarily proportional to the number of bedrooms).

Also, this rate might not be suitable where all facilities are not equally shared, such as mixed development projects, because functional unit is an item that uniformly represents the building, including main facilities and sub-facilities.

Exercise: Hospital project

A city hospital project had 200-bed capacity and cost $30,000,000. What would be the estimate of a similar city hospital project if it were going to have 110 beds?

Answer

Cost per functional unit (bed) = $30,000,000 ÷ 200

Cost per bed = $150,000

Estimated cost = $150,000 × 110 beds

= $16,500,000 ($16.5 million)

3.2.2 Area method

The area method is also a simple technique of cost planning. This method requires the total area of the building. Usually, the Gross Floor Area (GFA) is applied in this technique. This technique can be used for any building type, including the types where the functional unit cannot be identified.

Gross Floor Area (GFA): Definition

This is the main building area as a sum of all functional areas. There are slightly different definitions and measurement rules given in ACMM (2022) and by NZIQS (2017).

See Chapter 8 for more details about GFA, including measured examples.

Exercise: School project

A school project had a GFA of 850 m2 and cost $1,785,000. What would be the estimate of a similar school project if it had a GFA of 1,250 m2?

Answer

Cost per m2 GFA = $1,785,000 ÷ 850 m2

Cost per m2 GFA = $2,100

Total estimated cost = $2,100/m2 × 1,250m2

= $2,625,000

3.2.3 Functional area method

The functional area method is commonly used in the early cost planning stages.

Functional area (FA): Definition

‘Any group of accommodation that has a common work function within a particular type of a building. It includes all circulation necessary within that area’ (AIQS 2022, p. 6).

This technique can also be used in any type of building. Despite the common function of the building, various functional areas of a building serve different purposes, and the cost of constructing those functional areas can be varied due to factors such as the method of construction and types of finishes applied.

- In a hospital, bed-based service areas, administration areas and emergency departments are serving various functions related to the health service function of the building.

- In a school, classrooms, playrooms, laboratories and offices are serving various functions related to educational functions of the building.

- In residential buildings, wet areas such as bathrooms require waterproofing and tile finishes, whereas living areas can be finished with timber flooring. The types of finishes used are based on the different functional areas and the cost of construction varies.

Example: Boarding house project

| Ref. | Functional areas | Area (m²) | Rate ($/m²) | Cost |

|---|---|---|---|---|

| a) | Reception and office | 36 | 3,500 | 126,000 |

| b) | Bedrooms | 480 | 2,800 | 1,344,000 |

| c) | Bathrooms | 100 | 6,500 | 650,000 |

| d) | Plant and storage | 80 | 4,000 | 320,000 |

| e) | Circulation/Travel areas | 115 | 1,800 | 207,000 |

| Total Building Cost* | 2,647,000 |

*This example only indicates building cost based on the functional areas. Other cost components should be included in the cost plan to calculate the total project cost (See Chapter 6 and Chapter 7 for other costs).

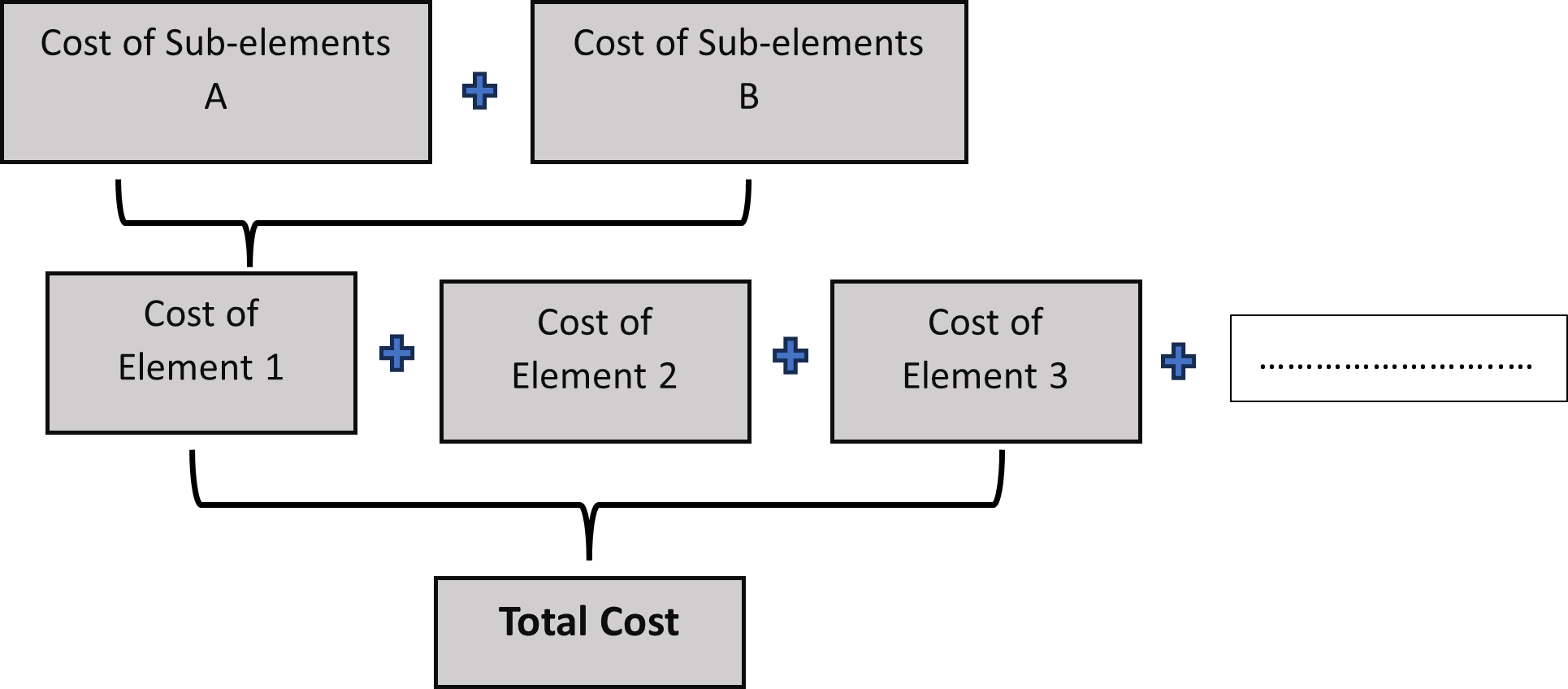

3.2.4 Elemental cost planning

An elemental cost planning is a budget-distributing technique that can be applied when more design information is available. It is based on an elemental breakdown of works and measurement of elements and sub-elements to which rates are applied.

Element: Definition

‘A portion of a project that fulfils a particular physical purpose irrespective of construction and/or specification’ (AIQS 2022, p. 5).

Sub-element: Definition

‘A part of an Element that is physically and dimensionally independent and separable in monetary terms’ (AIQS 2022, p. 11).

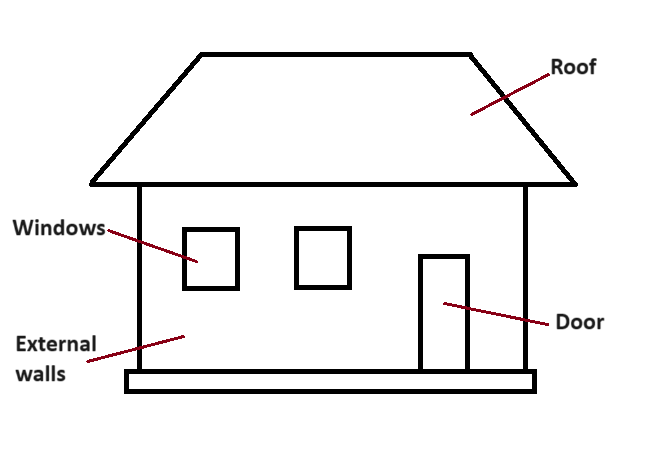

For example, the element ‘External Walls’ can be divided into sub-elements such as Brick Walls, Brick Veneer Walls, Concrete Block Walls, In-situ Concrete Walls and so on.

According to AIQS (2022), elemental cost planning can be started in a simple form when outline proposals are available. A detailed elemental cost plan can be then prepared in later stages when more details are available and further developed into a tender document cost plan.

Standard documents specify elemental breakdowns and define elements along with the unit of measurement and rules to measure elemental quantities. See Chapter 8 for a comparison of elemental breakdown between AIQS (2022) and NZIQS Elemental Analysis (2017).

Elemental quantity

If the necessary drawings are available, elemental quantities are measured in accordance with the definitions and measurement rules specified in a standard document (See Chapter 8 for measured examples). Otherwise, GFA will be used as the element unit quantity.

Elemental unit rate

Elemental Unit Rates are considered benchmark rates for cost planning and provide important cost information.

For example, experienced cost planners can determine whether an elemental rate is realistic for a given type of project in the market at current rates and compared to other benchmark buildings. This helps identify any errors in measurement of pricing .

Elemental cost

Elemental cost is the multiplication of Elemental Quantity and Element Unit Rate. The total cost of the building is then derived as the sum of all elemental costs as shown in Figure 3.3. This provides the basis for cost planning and cost controlling and facilitates value management practices.