Chapter 2: Cost Management of Building Construction Projects

2.0 Introduction

This chapter provides an overview of the concept of cost management and highlights the importance of cost planning in building projects. The chapter starts by identifying the goals of a construction project. The chapter then clearly defines the terms ‘price’, ‘cost’ and ‘value’ and highlights that each term has its own attributes in understanding the concepts in cost management. It also defines the term ‘Budget’ as the most common and important aspect of cost planning. Then the chapter briefly discusses the cost management process across different phases of a construction project. The chapter also briefly explains different procurement methods that can vary some activities in the cost management process.

2.1 Goals of a construction project

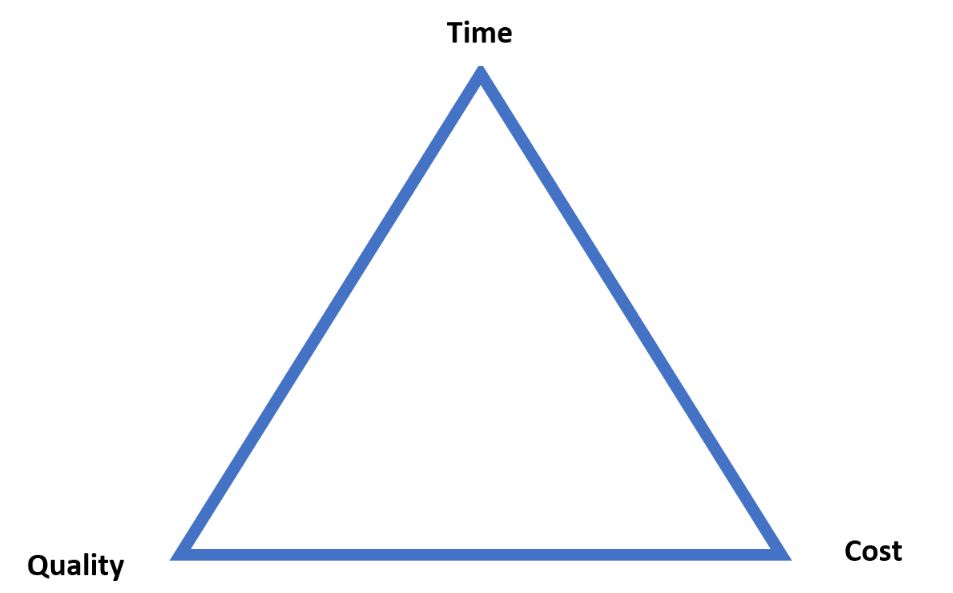

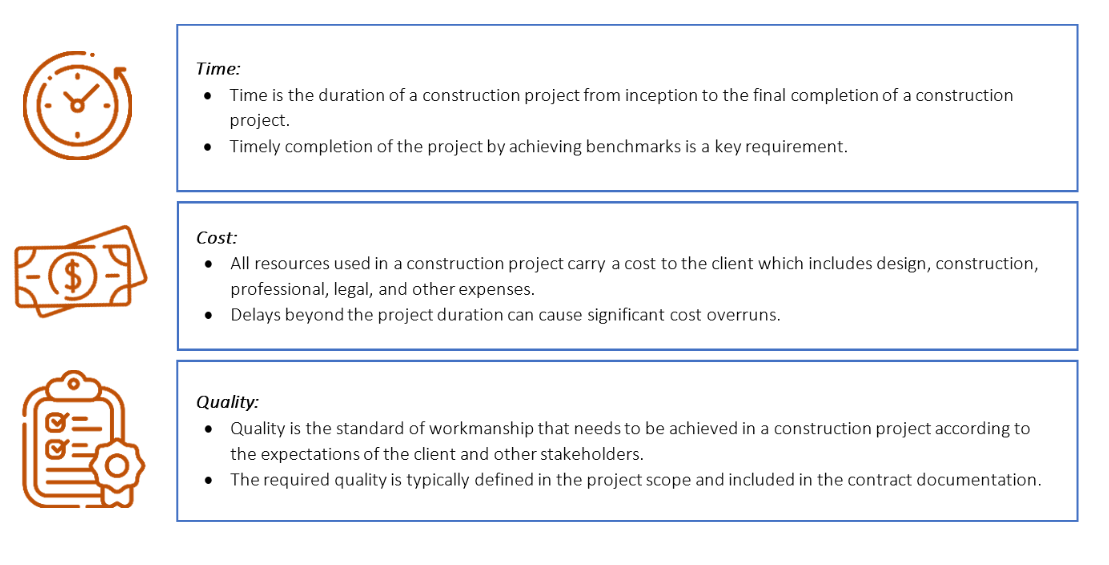

The client’s primary objectives for a construction project are to obtain the final product within the agreed cost, time, and quality targets. These objectives are interconnected and are clear benchmarks to judge a project’s success or failure. The relationships of these objectives can be illustrated in a triangle, often called the ‘golden triangle in construction‘. These 3 objectives are illustrated and explained in Figures 2.1a and 2.1b.

Clients do not have unlimited funds or time to achieve high-quality construction fulfilling their needs. Therefore, a construction project requires estimated time and cost limits when achieving the quality requirements, so the project is considered within the client’s acceptable limits. There are trade-offs between 3 objectives and the client can attain value for money in a project by balancing time, cost and quality. However, achieving these 3 objectives simultaneously is not a simple task and is known to be very complex.

Scenario: Balancing time, cost, and quality

- If a client wants to reduce construction time, it can be done by increasing the number of labourers and machinery in work. This will increase the cost of the work. However, new construction methods and technologies can be introduced to reduce the cost.

- Structural integrity is a must for a quality project and cannot be compromised by cost savings. If so, it will result in safety issues, and high maintenance costs. Using some economically advanced technologies could potentially change the specifications and provide an economically sound and effective structural design without compromising quality.

- The workmanship required for fine arts or finishes such as cornices, architraves, and other decorative elements consumes a considerable amount of time. The quality of these elements cannot be compromised due to the time required. However, by using precast elements instead of in-situ construction, time savings are possible.

Each resource used in a construction project carries a cost. The client is financing the project and the amount of money that the client has allocated or can afford for a project is known as the client’s ‘budget’. The rule of thumb is not to exceed the client’s budget. Hence, the cost can be identified as the governing factor of time and quality of construction.

2.2 ‘Price’, ‘cost’, ‘value’ and ‘budget’

Price, cost, value and budget are common terms when costing a construction project and sometimes are used interchangeably. However, each of these terminologies carries a different meaning in the construction industry. The difference occurs based on the client’s and contractor’s perspectives (see Figure 2.2). The contractor’s cost is all expenses incurred by the contractor for a given project. After adding the contractor’s profit to this cost, it becomes the client’s cost. This is known as the price that the client pays to the contractor. In cost planning, cost means the price to the client and it can include other costs to the client and goods and services tax (GST). The budget is what is available to spend for a project. Therefore, the cost to the client (price) should not exceed the client’s budget. In the cost planning process, the design may need to be refined to maintain the cost within the ‘budget’.

A project budget can be determined based on the availability of funds.

For public sector projects, government agencies set a project budget based on a master plan and budgetary allocation per financial year.

Scenario: State government budget

The below is an example of a state government in Australia announcing the budget allocated for a hospital project. The project’s cost planning should be undertaken within this announced budget.

‘The Victorian Government is investing $595 million to redevelop and expand the Ballarat Base Hospital.

The redevelopment will deliver a new emergency department, a women and children’s hub, state-of-the-art theatre suite and an extra 100 inpatient and short stay beds. A new and expanded critical care floor will bring together operating theatres, procedure rooms, an expanded intensive care unit, endoscopy suites and consulting rooms. This will deliver capacity for an additional 4,000 surgeries every year. Once completed, the upgraded hospital will have the capacity to treat at least 18,000 more emergency patients and an extra 14,500 inpatients per year.’

— Victorian Health Building Authority, 2024)

Private sector project budgets depend on financial capacity and lending capacity approved by lending agencies (i.e. banks).

Compared to ‘price’ ,’cost’ and ‘budget’, ‘value’ is a subjective term. Value is the perceived benefits or worth of construction to the client. Value of a construction project can be considered in terms of economic, social, environmental, political, aesthetic, moral and other factors. A commonly used term is the ‘economic value’ of the construction project. If the final project exceeds the client’s expectations at the minimum possible cost, then the maximum economic value can be attained.

2.3 What is cost management?

As explained in Chapter 1, construction projects are unique and complex in nature. Construction projects involve many resources and long durations compared to other industries which require careful management of cost.

Cost management: Definitions

‘The technique(s) used for managing the cost of a project from brief to final account.’

— AIQS (2022, p. 4)

‘Cost management of a project includes establishing the budget and then effectively monitoring and reporting against that budget on a regular basis, cost planning the evolving design, preparing appropriate contract documentation and advising on variations and claims during the progress of the project.’

— AIQS (2012, p. 11)

Cost management for a general project is ‘the processes involved in planning, estimating, budgeting, financing, funding, managing, and controlling costs so that the project can be completed within the approved budget’.

— Project Management Institute (2017, p. 231)

Cost management items related to the Quantity Surveyor’s role include ‘managing finances of any kind of project, keep work within time, and estimated budget; efficiently manage construction cost and production’.

— NZIQS (2023)

Based on these definitions, it is understood that cost management is a series of actions implemented in managing the cost of a project in different stages of the construction project, rather than a one-off activity. Therefore, we can simply say that cost management is a process of managing the cost of a project throughout the project’s life cycle. This process is usually explained throughout different stages of a project’s life cycle. Cost management might also be called ‘cost engineering’ in some countries.

2.3.1 Project stages

Different countries and regions follow standard documents or manuals providing categorisation of project stages and functions of each stage.

Royal Institute of British Architects (RIBA) Plan of Work

RIBA is a global professional body in architecture originated in UK. RIBA Plan of Work is a globally known framework that organises the process of managing building projects and administering building contracts. This framework is also followed by cost managers in the UK construction industry and most other countries in their cost management process. Royal Institution of Chartered Surveyors (RICS) has adopted the RIBA Plan of Work in their standards related to the cost management processes and presented in RICS New Rules of Measurement (2021).

OGC (Office of Government Commerce) Gateway Process

The OGC Gateway Process is an alternative to the RIBA Plan of Work by the Office of Government Commerce in UK. Some UK government departments and public sector organisations adopt this framework for designing and managing building projects.

Australian Cost Management Manuals (ACMM)

Australian Cost Management Manuals consist of a series of manuals published by the AIQS and endorsed by APCC for cost management of the construction process. They organise the cost management activities throughout a construction project following its stages.

New Zealand Construction Industry Council (NZCIC) Design Guidelines

NZCIC is a not-for-profit industry association of building, construction and property sector associations. Concerning the poor documentation prevailed in the New Zealand building industry, a committee endorsed by the NZCIC drafted the Design Guidelines. This document specifies the design process of ‘building’ projects in New Zealand providing general checklists and benchmarks.

Comparison of cost management stages in standard documents

Despite region-specific differences in terms, the standard documents mentioned in this section generally cover the key stages in the life cycle of a construction project. Table 2.1 compares the cost management stages as given in standard documents in UK, Australia and New Zealand.

| Royal Institute of British Architects: Plan of Work 2020 | Royal Institution of Chartered Surveyors: New Rules of Measurement 1 (2021) | Office of Government Commerce (OGC) | New Zealand Construction Industry Council | Australian Cost Management Manual | |

|---|---|---|---|---|---|

| Pre-design | Strategic Definition (0) | Rough order of cost estimate | Business Justification (1) | – | – |

| Preparation and Brief (1) | Order of cost estimate(s) (option costs)

Elemental cost estimate |

Delivery Strategy (2) | Project establishment | Brief (A) | |

| Design Brief and Concept Approval (3A) | |||||

| Design | Concept Design (2) | Formal cost plan 1 | Concept Design | Outline Proposals (B) | |

| – | – | – | Preliminary Design | – | |

| Spatial Coordination (3) | Formal cost plan 2 | Detailed Design Approval (3B) | Developed Design | Sketch Design (C) | |

| Technical Design (4) | Formal cost plan 3 | Detailed Design | Documentation (D) | ||

| Investment Decision (3C) | |||||

| Contractor Engagement (part of the technical design stage) (4) | Pre-tender estimate

Pricing documents (for obtaining tender prices) Post-tender estimate |

Procurement | Tender (E) | ||

| Manufacturing and Construction (5) | – | Construction Adminstration and Observation | Construction (F) | ||

| Handover | Handover (6) | Formal cost plan (renew/maintain) | Readiness for Service (4) | Post Completion | |

| In use | In use (7) | (Measured in accordance with NRM 3) | Operations Review and Benefits Realisation (5) | – | – |

| End of life | – | – | – | – | – |

Pre-design stage/s

Pre-design stage/s provide the project set-up and involve actions before the actual design starts. Client’s requirements are communicated in this phase. NZCIC Design Guidelines and the ACMM cover pre-design activities in a single stage. In contrast, RIBA Plan of Work and RICS standard documents cover those in 2 stages. OGC Gateways standard, on the other hand, includes three stages for the pre-design activities, in which the third stage finalises the pre-design stage and continues to the design stage.

Design

Despite different terminologies, all these standard documents show similar categorisations of design stages, except the NZCIC guidelines having a separate stage for preliminary design and the OGC Gateways standard having 3 stages starting from pre-design and also covering the construction stage. The design stages include vital activities in the pre-construction phase in which the design is developed from concept/outline designs to detailed designs. The actual design development can involve several stages until the design is finalised and lead to complete documentation for tender, concluding most of the activities in the pre-construction phase.

Construction

Construction is usually covered through a single stage. Since RICS standard documents focus on cost estimating and planning which are pre-construction cost management activities, they do not mention the construction stage. Yet, the ACMM covers the cost management process and, hence, includes the construction stage.

Handover, In Use and End of Life

RIBA, RICS, OGC Gateways and NZCIC standards contain a separate stage for handover. NZCIC and ACMM do not contain an in use stage. Even though the construction industry practices require whole life cycle costing, including end-of-life work, none of these standards contain this stage yet.

Note: This book follows the cost management stages given in ACMM and NZCIC.

The steps in this section are mostly aligned with the six stages from Stage A to Stage F, presented in the ACMM (Volume 1) cost management line diagram. The line diagram shows the cost management activities carried out in each stage and the output which will be documented and presented to the client.

This line diagram is presented in the Appendix of this book and will be referred to throughout the book.

2.3.2 Cost management process activities

This section covers major steps in the cost management process.

Cost budgeting

According to the ACMM Volume 1 (2022, pp. 4) ‘cost budgeting is a method of arriving at the sum of money within which it is expected that the project will be cost planned’. This activity is done at the very beginning of the cost management process to establish the initial budget. Generally, the project design team is responsible for establishing the budget.

Cost planning

The ACMM Volume 1 (2022, p. 4) defines cost planning as:

a systematic application of Cost Management to the design process between Brief Stage Cost and pre-tender estimate with the purpose of establishing, regulating and reconciling the Project Cost.

Cost planning is not a one-off activity, but a process carried out through the pre-construction cost management stages in line with the design development stages to identify the costs of a construction project. Therefore, different cost planning techniques are used at each stage based on the availability of design details and project information in each stage. At the initial stages, the budget can be expressed as a range due to lack of certainty and will become more accurate with more details in the later stages. Cost planning helps a project achieve acceptable value for money, valuing project risks by creating budgets and cost plans, comparing costs of different alternatives, and controlling the budget throughout the project.

Client’s quantity surveyor/cost planner carries out the cost planning activities. However, it needs the continuous involvement of the project design team and other consultants (i.e. services engineers) to provide relevant details and cost components to update the cost plan with the design development.

Tendering

After the design development and cost planning processes, documentation will be completed and the tendering will take place to select the contractor/builder to carry out the construction work. The process is also known as ‘bidding’ and the competitive contractors/builders will be referred to as ‘tenderers’ or ‘bidders’.

This process generally involves:

- developing tender documents

- calling tenders, or inviting preselected bidders

- contractors filling the bidding documents together with the estimate developed by the contractor’s/builder’s estimator (providing the price offered)

- bidders visiting the site

- providing additional information to contractor queries

- bidders submitting completed bidding documents for evaluation

- evaluating the bidding documentation by client’s team and selecting the suitable contractor

- final negotiations and signing the contract.

However, there are variants based on the procurement method and types of contracts such as selecting the contractor and negotiating the contract later.

Cost estimating

Cost estimating should not be misunderstood with cost planning. The term ‘estimating’ is used interchangeably during cost planning but mostly refers to the pricing of a project by the contractor’s/builder’s estimator to submit as a part of bidding documents.

Cost controlling

Construction projects are unique and complex in nature and involve many uncertainties. Therefore, variations are common in construction projects due to various reasons including changes to client’s needs and unforeseeable circumstances. These will impact the project time, cost and quality. After an initial budget has been developed and accepted, cost controlling process would apply for a project. Cost control processes are applied to keep the final cost of the project within the acceptable cost ranges. With the progression of the project, the actual and estimated cost should be compared and the cost plan should be updated. If the cost of the project exceeds or is projected to exceed accepted levels, the client should be informed and action should be taken to make changes to the project construction and procurement process to bring the project to acceptable levels or change the acceptable levels.

It is understood that cost controlling should be conducted so an acceptable budget has been identified and not wait until the construction starts. This is because it is easy to make changes to the project at the initial stages of the project with less cost impact compared to the latter stages. Some changes might require rework, which would impact both project cost and time and require more work to be done in less time.

Final accounts

Final account reflects the final agreed cost of the construction project. Final accounts are developed at the end of the construction project after all work is completed. There will be no changes to the final cost of the construction project after the final accounts have been completed. The final accounts are first developed by the contractor/builder and evaluated by the client or client’s representative. All parties to the contract should agree to the cost to be final accounts. When there are multiple contracts to a project, final accounts of all the contracts will be the final accounts of the project. Until final accounts are developed and finalised, all valuation payments for work done are subject to change.

Cost analysis

According to the Building Cost Information Service (BCIS) (2012, p. 9):

the purpose of cost analysis is to provide data that allows comparisons to be made between the costs of achieving various building functions in a project with those of achieving equivalent functions in other projects.

Cost analysis can be considered as the process of analysing cost data from previous projects so that those data can be used in the cost planning and estimation of new projects.

Standard documents such as BCIS of RICS, ACMM and NZIQS elemental analysis of costs of building projects provide the basis for a systematic cost analysis following the elemental breakdown of building costs. The documents used to prepare the cost analysis should be stated. More often, this is the agreed price for the works – i.e. the priced bill or schedule of prices.

Chapter 5 is about cost analysis of construction projects.

2.3 Procurement methods

The term ‘procurement’ has broader meanings, but procurement methods in construction explain the contractual arrangements, project financing and payment methods. The selected procurement method for a project affects the cost management process and builder’s involvement in different stages. Several characteristics of procurement methods that are commonly used in Australia and New Zealand are discussed below.

Traditional method/Construct only

- Client is responsible for the design and construction documentation and has the full control of the design and project outcome.

- Client engages consultants to undertake full design and documentation.

- Competitive tendering is carried out using the design and documents to select a contractor.

- Cost of tendering for contractors is low due to no design exercises involved during tendering.

- The selected contractor carries out the construction work only.

- Payment is usually based on a lump sum fixed price.

Design & Construct (D&C)

- Client engages a design consultant to prepare a concept or schematic design.

- This schematic design is provided to tenderers to develop as part of the tender process to inform the tender price and program.

- Cost of tendering for contractors may be higher due to cost of design and higher due diligence.

- Contractor is engaged to complete the detailed design and construct the project.

- Contractor bids a program that becomes the agreed baseline for the project.

- Payment method can be a combination of lump sum fixed price, schedule of rates, cost reimbursement, and target cost. A sharing of savings and overruns can involve.

- Contractor is responsible for design and constructability and has greater involvement over the design outcome.

Early Contractor Involvement (ECI)

- Client develops a functional brief which informs a concept or schematic design, and a pre‑tender cost estimate for construction.

- Contractors bid a fixed price to develop schematic and/or detailed design during the design phase.

- Cost of tendering is lower because the single contractor is paid a fee for participating.

- Payment is usually based on a lump sum fixed price.

- Collaboration between the contractor and client on design may lead to better overall design outcomes.

Managing contractor

- Client engages a design consultant to prepare concept design.

- Competitive tendering process is used to select a Managing Contractor based on preliminaries, and design and management fee.

- Managing contractor designs the project with client’s input and coordinates the construction and project delivery.

- Cost of tendering for contractors is lower compared to D&C mode as there is no up-front tender design involved.

- Subcontract trade packages are competitively tendered by the Managing Contractor.

- Payment is usually based on a lump sum fixed price for Managing Contractor, reimbursement of subcontractor, target cost with a share of gain/pain.

- Greater client influence and input in design, constructability and delivery, reducing the risk that the client’s requirements will not be met.

The lump sum fixed payment is applicable for all available methods, given the well-defined project scope. Procurement methods such as construct-only, ECI, D&C and managing contractor use a lump sum fixed price method. While providing the client with the most certainty by minimising the risk of capital expenditure, it allocates most of the risk to the main contractors. In contrast, D&C and managing contractor do not purely rely on a fixed price lump sum method; thus, they follow a combined payment method to reduce the contractor’s risk.

Did you know?

Compared to Construct Only, the ECI outcome was considered extremely successful, and the projects were delivered ahead of the contract program and on budget in a COVID-19 environment. The significant involvement of the builder maximises the value for money and improves end-year outcomes.

However, in general, the majority of public sector building construction projects follow the traditional/construct-only method, as the government, as a client, can maintain significant control over the projects.